Table of Contents >> Show >> Hide

- The Simple Answer: VCs Need Big Winners To Return Their Funds

- Why “Just Making Money” Is Not Enough For A VC

- The Power Law: Venture Capital Is Not Averages; It Is Outliers

- Why Fund Size Changes Everything

- Ownership, Valuation, And Dilution: The Founder’s Triangle

- Why VCs Care About Pro Rata Rights

- Why Preferred Stock Gives VCs More Than Common Equity

- Why Board Seats Often Follow Ownership

- Why Founders Should Not Automatically Fear Dilution

- When VC Ownership Demands Become Too Much

- What Founders Can Do Before Negotiating With VCs

- Experience-Based Notes: What Founders Often Learn The Hard Way

- Conclusion

Venture capital can feel like a glamorous dinner party where everyone talks about billion-dollar outcomes, “category creation,” and “changing the world,” while the founder is quietly staring at the term sheet thinking: “Wait… you want how much of my company?”

That reaction is normal. When a VC asks for 10%, 15%, 20%, or even 25% ownership, it can feel aggressiveespecially if you have spent years building the product, recruiting the team, finding customers, and surviving on coffee, optimism, and one suspiciously old protein bar in your desk drawer.

But VCs are not usually asking for meaningful ownership because they enjoy watching founders sweat through spreadsheets. They do it because venture capital has a very specific economic model. The math is unforgiving, the failure rate is high, and a small number of winners must pay for a large number of losses. In other words, VC ownership targets are not random. They are the engine that makes the venture business work.

This article explains why VCs want to own so much when they invest, how fund economics shape startup financing, what founders should understand before raising capital, and how to negotiate without turning the meeting into a financial cage match.

The Simple Answer: VCs Need Big Winners To Return Their Funds

The core reason VCs want significant ownership is simple: they need the upside from a few breakout companies to make the entire fund successful.

A venture fund might invest in 20, 30, or 50 startups. Most of those companies will not become huge. Some will fail. Some will return a little money. A few may become solid businesses but not large enough to move the fund. Then, ideally, one or two companies become massive outcomes. Those winners need to generate enough profit to cover the losers, reward the limited partners who invested in the fund, and justify the risk of backing early-stage companies in the first place.

That is why VCs often talk about whether an investment can “return the fund.” If a VC manages a $100 million fund, one great investment that produces $100 million in proceeds can return the original fund size. Everything else after that can help create the actual profit.

Now imagine the VC owns only 2% of a company. Even if that company sells for $500 million, the VC’s stake is worth only $10 million before considering dilution, fees, and fund mechanics. That is a nice result, but it does not move a large fund very far. If the VC owns 20% of that same company, the stake is worth $100 million. Suddenly, one exit can reshape the fund.

That is the heart of the issue. Small ownership can produce good headlines. Meaningful ownership can produce fund-level returns.

Why “Just Making Money” Is Not Enough For A VC

Founders sometimes ask: “If I turn your $2 million investment into $10 million, isn’t that great?” In normal life, yes. Turning $2 million into $10 million is wonderful. Most people would celebrate with a nice dinner, a responsible savings plan, and perhaps an unnecessarily large espresso machine.

In venture capital, however, the bar is different. VCs are not trying to make ordinary returns. Their investorscalled limited partners, or LPscommit capital to venture funds because they expect higher returns than they could get from safer assets. Venture is risky, illiquid, and slow. Money may be locked up for ten years or more. LPs are not donating to the “Let’s See What Happens” foundation. They expect venture-scale results.

That means a VC fund often aims to return multiple times the capital it raised. A fund that only returns the original capital is usually not considered successful. A fund that returns two times capital may be acceptable in some contexts, but many venture managers aim much higher. To get there, the best companies in the portfolio must create outsized returns.

The Power Law: Venture Capital Is Not Averages; It Is Outliers

Venture returns follow what investors often call the power law. In plain English, this means a tiny number of companies create most of the gains. Venture capital is not like buying a basket of stable dividend stocks where many holdings contribute evenly. It is more like fishing in a lake where 49 fish are normal size and one fish is wearing sunglasses, driving a speedboat, and worth $10 billion.

Because outcomes are so uneven, VCs care intensely about owning enough of the rare winners. A fund can have many investments that look promising, but if the winning company is owned at too small a percentage, the fund may still underperform. That is why ownership percentage is not a vanity metric. It is a survival metric.

For founders, this explains why a VC might pass on a deal even if the company is attractive. If the round is too small, the valuation too high, or the available allocation too tiny, the VC may not be able to own enough for the investment to matter to the fund. The company could still be great. It simply may not fit that investor’s fund math.

Why Fund Size Changes Everything

The bigger the VC fund, the more ownership pressure it usually has.

A small pre-seed fund may be able to generate an excellent return by owning a smaller stake in a company that exits for a few hundred million dollars. A large Series A or growth fund may need much larger outcomes or much bigger ownership to make the same investment meaningful. This is one reason founders sometimes hear different ownership expectations from different investors.

Small Funds

Seed funds often write smaller checks and may target around 10% ownership, although this varies widely by market, company quality, competition, and round structure. A seed investor can win if it enters early, gets a good price, and follows on selectively in the best companies.

Larger Funds

Larger venture funds may want 15% to 25% ownership because their checks are bigger and their return requirements are heavier. If a fund is hundreds of millions or billions of dollars, a small stake in a modest exit is not enough. The investment must have a path to becoming a major return driver.

This is why a big VC may offer more money than a startup originally planned to raise. It may not be because the founder needs all of that capital immediately. It may be because the investor needs to write a large enough check to reach its target ownership.

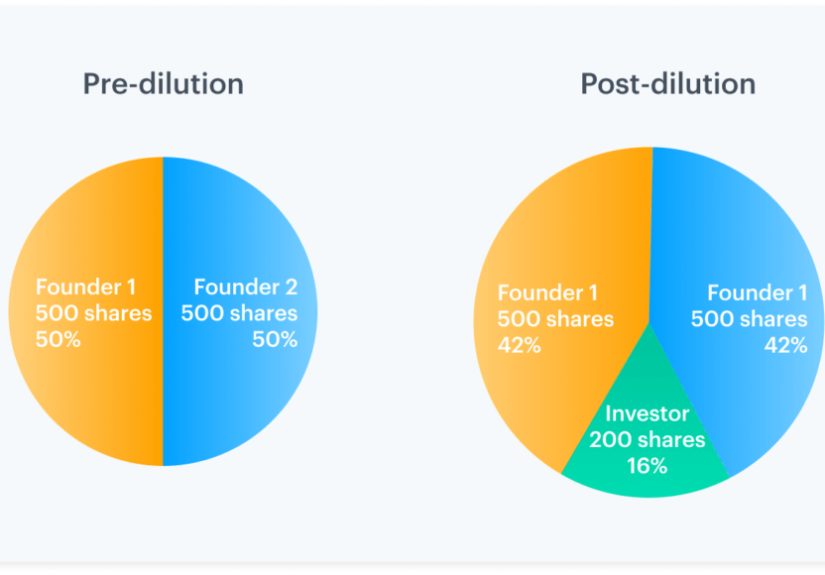

Ownership, Valuation, And Dilution: The Founder’s Triangle

When founders negotiate with VCs, three concepts are always dancing together: valuation, round size, and dilution.

If you raise more money at the same valuation, you sell more of the company. If you raise the same amount at a higher valuation, you sell less. If you raise less money, you may preserve more ownership, but you might also risk underfunding the business. Like most startup decisions, there is no free lunchonly a lunch someone later calls “strategic capital allocation.”

For example, suppose a company raises $5 million at a $20 million post-money valuation. Investors own 25% after the round. If the company raises $5 million at a $25 million post-money valuation, investors own 20%. If the company raises $3 million at a $20 million post-money valuation, investors own 15%.

Founders often focus on valuation because it feels like the scoreboard. But dilution may matter more over the long term. A slightly lower valuation with the right partner and enough capital to reach the next milestone can be better than a shiny valuation that leaves the company underfunded, over-pressured, or stuck with poor terms.

Why VCs Care About Pro Rata Rights

Ownership is not just about the first check. VCs also care about keeping their ownership over time.

When a startup raises future rounds, existing investors are diluted unless they invest more money. Pro rata rights give investors the ability to participate in future financing rounds to maintain their percentage ownership. This matters because the best startups usually raise multiple rounds before reaching an exit.

From the VC’s perspective, pro rata rights protect access to the winners. Imagine investing early in a company that suddenly becomes the hottest startup in the market. Without pro rata rights, later-stage investors might crowd out the early investor. With pro rata rights, the early investor can keep supporting the company and preserve a meaningful stake.

From the founder’s perspective, pro rata rights can be helpful because they signal existing investor confidence. But they also affect future financing flexibility. If too many investors have large pro rata rights, a future round can become crowded before new investors even enter the room.

Why Preferred Stock Gives VCs More Than Common Equity

VC ownership is not always the same as founder ownership. Founders and employees usually hold common stock. VCs usually receive preferred stock, which often comes with special rights.

These rights may include liquidation preferences, anti-dilution protections, information rights, voting rights, board rights, and other investor protections. The most common and important is the liquidation preference, which helps determine who gets paid first if the company is sold or liquidated.

This does not mean every VC term sheet is evil. Many investor protections are standard, and modern venture financing documents are often built around familiar market norms. Still, founders should understand that selling 20% of the company to preferred investors is not the same as giving someone 20% of plain common stock. The rights attached to the shares matter.

Why Board Seats Often Follow Ownership

VCs also want ownership because it justifies the time and responsibility of being deeply involved.

A partner at a venture firm can only sit on so many boards and actively help so many companies. Board work is not just attending meetings and nodding thoughtfully while pretending the Wi-Fi is stable. It includes recruiting executives, helping with future fundraising, advising on strategy, dealing with crises, reviewing budgets, and supporting the founder through difficult decisions.

If a VC owns a tiny percentage, it may be hard to justify that level of attention. If the VC owns a meaningful stake, the economics support deeper involvement. This is why ownership, board participation, and investor engagement are often connected.

Why Founders Should Not Automatically Fear Dilution

Dilution is not always bad. Bad dilution is bad. Useful dilution can be excellent.

If selling 20% of your company gives you the capital, credibility, network, and runway to turn a $10 million business into a $1 billion company, that dilution may be a bargain. Owning 60% of a tiny company is not automatically better than owning 30% of a giant one.

The key question is not simply, “How much am I giving up?” The better question is, “What does this capital help me build, and does the trade-off increase the value of my remaining ownership?”

Founders should think in terms of outcome value, not just percentage ownership. A smaller slice of a much larger pie can be better. Of course, this assumes the pie actually gets larger. If the capital is wasted, the investor is unhelpful, or the company raises at unsustainable prices, dilution can become painful very quickly.

When VC Ownership Demands Become Too Much

Not every ownership request is fair. Sometimes a VC asks for too much because the company has limited options, the market is weak, the business is risky, or the investor is simply pushing hard.

Founders should be cautious if a round would leave them demotivated, make future financing difficult, or create a cap table that looks like it was assembled during a thunderstorm. Excessive early dilution can hurt hiring, reduce founder incentive, scare later investors, and make future option pool planning harder.

A useful rule of thumb is to model several rounds ahead. Do not only ask what your ownership looks like after this round. Ask what it could look like after the next two or three rounds, including option pool increases and pro rata participation. A term sheet that looks acceptable today may feel much less friendly after Series B, Series C, and a down round cameo appearance no one invited.

What Founders Can Do Before Negotiating With VCs

1. Understand Your Milestones

Raise enough money to reach a meaningful next milestone. That milestone might be revenue growth, product launch, enterprise traction, regulatory progress, or a strong Series A profile. Raising too little can force you back into the market before you have improved the company’s value.

2. Build A Dilution Model

Model your cap table across multiple rounds. Include option pools, SAFEs, notes, priced rounds, and future hiring needs. This does not require wizard-level finance skills, but it does require honesty. Spreadsheets are cheaper than regret.

3. Compare More Than Valuation

The highest valuation is not always the best deal. Compare ownership sold, investor quality, board structure, liquidation preference, anti-dilution terms, pro rata rights, and how much help the investor can realistically provide.

4. Ask Investors About Their Ownership Requirements

It is perfectly reasonable to ask a VC what ownership range they typically target. This can save time. If you want to sell 12% and the investor needs 25%, you have discovered a mismatch earlybefore everyone spends three weeks exchanging polite emails that translate to “this will never happen.”

5. Choose Capital That Matches Your Ambition

VC money is designed for companies that can become very large. If you want to build a profitable, steady, founder-controlled business, venture capital may not be the best fit. That is not a failure. That is strategy. Not every great company needs venture capital, and not every venture-backed company becomes great.

Experience-Based Notes: What Founders Often Learn The Hard Way

In real fundraising conversations, founders often begin by treating ownership as a battle: founder versus VC, builder versus spreadsheet, hoodie versus Patagonia vest. But the better way to look at it is alignment. A good VC wants enough ownership to make the investment matter. A good founder wants enough ownership to stay motivated and enough capital to win. The best deals sit in the middle, where both sides can look at the outcome and say, “Yes, this can work.”

One common experience is that founders underestimate how much future dilution will happen. The first round feels like the big event, but it is rarely the last one. A startup may raise seed, Series A, Series B, Series C, and possibly extension rounds. Each financing can add new dilution. Option pools may need to be refreshed to hire senior talent. SAFEs and convertible notes may convert in ways that surprise founders who did not fully model them. By the time the company reaches scale, the original ownership picture can look very different.

Another practical lesson: the investor’s fund size explains much of the negotiation. A founder may pitch a large multi-stage fund and wonder why the investor is pushing to write a bigger check than needed. The answer is often not mysterious. The fund has to deploy significant capital and own enough for the investment to matter. The same company might receive a very different proposal from a smaller seed fund, angel syndicate, or strategic investor.

Founders also learn that dilution hurts less when the money is tied to a clear plan. Raising $4 million to reach $1 million in annual recurring revenue, hire two key engineers, and launch a repeatable sales process is very different from raising $4 million because “more runway sounds comforting.” Capital should buy progress. If it only buys time, the company may return to the market with the same story and a lower ownership percentage.

The best founders enter VC discussions prepared but not defensive. They know their numbers, understand their milestones, and ask direct questions. What ownership does the fund need? How much follow-on capital can it reserve? What does the partner do after investing? How does the firm behave when things go sideways? These questions reveal whether the VC is merely buying equity or actually becoming a long-term partner.

Finally, experienced founders understand that ownership is emotional because startups are personal. You are not selling shares in a spreadsheet. You are selling a piece of something you created. That deserves respect. But emotion should not block clear thinking. The goal is not to preserve every percentage point at all costs. The goal is to build the most valuable company possible while keeping the team, investors, and incentives aligned. In the end, great venture deals are not about who “wins” the negotiation. They are about whether the company gets the fuel, support, and structure it needs to become big enough for everyone’s ownership to matter.

Conclusion

VCs want to own so much because venture capital is built on extreme outcomes. Most startups will not produce fund-changing returns, so the few that do must be large enoughand owned meaningfully enoughto carry the portfolio. Ownership targets are shaped by fund size, return expectations, dilution, pro rata rights, board involvement, and the power-law nature of startup investing.

For founders, the lesson is not “avoid dilution at all costs.” The lesson is to understand what you are trading. If a VC asks for 20%, the right response is not panic. It is analysis. What capital do you need? What milestone will it fund? What terms come with it? What partner are you getting? What will your cap table look like after future rounds?

The best fundraising decisions balance ambition with discipline. Sell enough equity to give the company a real shot at becoming huge, but not so much that founders, employees, or future investors lose confidence in the journey. Venture capital is expensive money, but when used well, it can turn a promising startup into a market-defining company. Just make sure you understand the math before signing the term sheetbecause in venture, the percentage points may look small, but they have very long shadows.