Table of Contents >> Show >> Hide

- The Short Answer: Yes, the Wealth Gap Is That Big

- What Wealth Inequality Actually Means

- Why Wealth Inequality in America Feels So Extreme

- How the Wealth Gap Shows Up in Everyday Life

- Is Wealth Inequality Getting Worse, or Better?

- What Would Actually Shrink the Wealth Gap?

- What Wealth Inequality Feels Like in Real Life

- Conclusion

Let’s skip the polite throat-clearing and get to it: wealth inequality in America is very bad. Not “hmm, that seems a little lopsided” bad. More like “some people are buying a third vacation home while someone else is stress-calculating a $400 car repair” bad. And that distinction matters, because wealth is not the same thing as income. Income pays this month’s bills. Wealth buys breathing room, second chances, better neighborhoods, safer retirements, and the ability to survive a financial surprise without immediately entering a panic spiral.

That is why the debate over wealth inequality in America is not just about billionaires, yachts, or whether anyone really needs a fridge with Wi-Fi. It is about who gets stability and who gets fragility. It is about who can afford risk, who can pass opportunities to their kids, and who has to spend most of life one bad break away from financial chaos. If you want the most honest answer to the question in this article’s title, here it is: America’s wealth gap is not a side issue. It is one of the central facts shaping modern American life.

The Short Answer: Yes, the Wealth Gap Is That Big

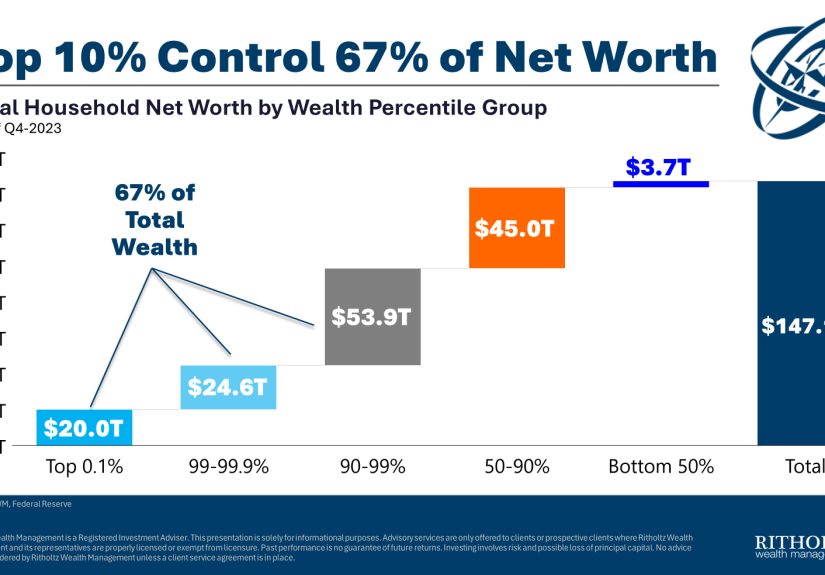

By one of the clearest modern measures, the top 1% of U.S. households now hold roughly a third of all household wealth, while the bottom 50% hold only a tiny sliver. Put less politely, a very small club owns a huge chunk of the pie, and half the country is left arguing over crumbs. That alone tells you a lot about how wealth concentration in America works.

Even when economists use a broader method that counts projected Social Security benefits, the picture is still harsh. On that measure, the top 10% of families hold about 60% of all wealth, while the bottom half hold just 6%. So whether you use the stricter market-wealth lens or the more expansive one, the conclusion barely changes: the distribution is deeply unequal. In technical terms, the methods differ. In plain English, the economy still looks like it has a penthouse, a basement, and not much middle stairwell.

Another eye-opening number comes from the Census Bureau: median household wealth in 2023 was $191,100. That may sound respectable until you look around it. The 10th percentile sat at zero dollars or less, while the 90th percentile was above $1.8 million. That is a massive spread. So when people say the “average” household is doing fine, it is worth asking which household they have in mind. The answer is often: not the one sweating in the parking lot before checking their bank app.

What Wealth Inequality Actually Means

Before going further, it helps to define the thing properly. Wealth is what you own minus what you owe. It includes assets like a house, retirement accounts, savings, stocks, and business ownership, minus debts such as mortgages, credit cards, car loans, and student loans. Income is money flowing in. Wealth is the cushion already built.

That cushion changes everything. A family with solid wealth can survive a layoff, move for a better job, help a child with college, or put down a home deposit. A family with little or no wealth may have a similar paycheck on paper, but one broken appliance or medical bill can knock the whole month sideways. That is why the wealth gap in America matters more than many casual conversations admit. Wealth is not just money. It is resilience, leverage, and time.

Why Wealth Inequality in America Feels So Extreme

1. Asset booms reward people who already own assets

One of the biggest engines of American wealth inequality is simple: when stocks, businesses, and real estate rise, the people who already own them get richer. That sounds obvious because it is. But the consequences are enormous. The top 1% hold about half of corporate equities and mutual fund shares, which means that when financial markets soar, the gains land heavily at the top. The stock market may be reported like a national mood ring, but in reality it rewards households very unevenly.

Middle-class families are more likely to build wealth through housing and retirement accounts. Those are important assets, but they do not always appreciate the same way concentrated business equity or large stock holdings do. So while many households benefit somewhat when the economy expands, high-wealth households often benefit far more. The escalator moves for everyone; it just moves much faster for the people already standing near the top.

2. Homeownership helps build wealth, but access is unequal

Homeownership still matters a great deal in the United States. Census data show homeowners had about 48 times the median wealth of renters in 2023. That number is almost cartoonishly large, but it captures a real truth: owning a home remains one of the most common ways Americans build wealth over time.

Still, the story is not as simple as “just buy a house.” The Cleveland Fed has noted that homeownership can help lower-income households build wealth, but it also carries more risk for them than for high-income households. If your budget is already tight, a broken roof, job loss, or interest-rate shock can turn a wealth-building tool into a stress machine with siding.

And access is not equal. Treasury and Brookings have both emphasized that housing and homeownership gaps are major drivers of the racial wealth gap. Brookings notes that Black homeownership remains far below white homeownership, which limits one of the most important channels for building and passing down wealth. So yes, housing matters. But America has never handed out the keys evenly.

3. Race and history are still doing economic damage

If you want to understand how bad wealth inequality is in America, you cannot dodge the racial dimension. Pew Research Center found enormous wealth gaps between racial and ethnic groups even within the same income tiers. In 2021, the typical White household had far more wealth than the typical Black or Hispanic household, and the gaps did not vanish just because households earned similar incomes. That point is crucial. This is not only a story about paychecks. It is also a story about accumulated advantage, inherited disadvantage, and different starting lines.

Brookings put it especially bluntly: in 2022, for every $100 in wealth held by white households, Black households held only $15. That is not a rounding error. That is a structural divide. Historical barriers such as slavery, segregation, redlining, discrimination in labor and credit markets, and unequal access to appreciating assets still echo loudly in today’s balance sheets.

And the effects stack. Lower-income White households had vastly more wealth than lower-income Black households. That means two families can both be “working class” and still have very different levels of stability, options, and inherited support. One household may be poor with a cushion. Another may be poor with no buffer at all. Economically, those are very different universes.

4. Inheritance and tax rules quietly widen the gap

Wealth inequality is not only about who earns the most. It is also about who gets to keep, grow, and pass on assets most efficiently. The Center on Budget and Policy Priorities notes that the federal estate tax now affects fewer than 1 in 1,000 estates. In other words, the tax that is supposed to touch giant inheritances barely brushes the truly huge piles of money. That is not exactly a guillotine for dynastic wealth. It is more like a very polite tap on the shoulder.

CBPP also points out that unrealized capital gains make up a significant share of the assets in very large estates. Meanwhile, the Tax Policy Center notes that the tax treatment of capital income differs across asset types, and high-wealth families are more likely to own the kinds of assets that receive more favorable treatment. So the system does not merely reflect inequality; in some ways, it helps preserve it.

That is one reason wealth concentration is so sticky. Once wealth gets large enough, it can start behaving like a self-reinforcing machine. It earns returns, enjoys tax advantages, purchases advice, avoids distress sales, and then gets handed to the next generation. If regular families are running a financial relay race, many wealthy families begin several laps ahead and already own better shoes.

How the Wealth Gap Shows Up in Everyday Life

The biggest mistake people make is thinking wealth inequality is only visible in Forbes lists. It is not. It shows up in emergency savings, housing stability, education choices, retirement security, and the ability to recover from setbacks. The Federal Reserve found that in 2024, only 63% of adults said they could cover a $400 emergency expense completely with cash or its equivalent. Thirteen percent said they could not pay it right now. Thirty percent said they could not cover three months of expenses by any means if their primary income disappeared.

That is what economic inequality in the United States feels like on the ground. It is not always dramatic. Often it is quieter than that. It is postponed dental work. It is carrying credit card debt because the transmission died. It is saying no to a child’s summer program because the money has to stay liquid. The wealth gap is not just a chart. It is a thousand ordinary compromises.

Is Wealth Inequality Getting Worse, or Better?

The honest answer is: both, depending on what exactly you measure. Some data from the pandemic era show that many households experienced real gains in income, net worth, and savings. The Federal Reserve’s Survey of Consumer Finances found broad-based improvements between 2019 and 2022, with gains across many demographic groups. That matters, and it should not be ignored. It would be lazy to pretend nothing improved.

But level differences still remain enormous. That is the key. A household rising from almost nothing to a little more than almost nothing is still very vulnerable. A top-decile household growing from several million dollars to even more several million dollars remains in a different universe. So yes, some measures improved at the middle and bottom in recent years. But the underlying architecture of wealth inequality in America remains brutally concentrated.

Urban Institute researchers have argued that wealth inequality in the United States is higher than in almost any other developed country and has risen for much of the past several decades. That broader context matters. America is not merely unequal because some people are richer than others. Every society has that. America is unusual in how intensely wealth is stacked, how often that stacking follows race and class lines, and how much life opportunity depends on private household assets rather than public cushioning.

What Would Actually Shrink the Wealth Gap?

There is no single magic lever. Anyone promising a one-step fix is either selling a slogan or auditioning for a cable news segment. But the research points toward a consistent theme: if America wants less wealth inequality, it needs broader ownership of wealth-building assets, not just slightly nicer speeches about hard work.

That means stronger pathways into sustainable homeownership, especially for households historically excluded from it. It means retirement savings systems that do not depend so heavily on having a good employer and extra room in the monthly budget. It means policies that help families build emergency reserves and avoid high-cost debt traps. It also means looking seriously at how the tax code treats capital gains, inheritances, and asset income, because those rules shape how wealth compounds over time.

In other words, reducing wealth inequality in America is not mostly about punishing success. It is about deciding whether wealth-building should remain heavily reserved for people who already have wealth. Right now, the answer often looks like yes.

What Wealth Inequality Feels Like in Real Life

Here is the part that statistics cannot fully capture: wealth inequality has a texture. It has a feeling. It changes how people move through ordinary days.

Imagine two households with similar annual incomes. On paper, they may look close enough to be neighbors in a spreadsheet. But one family has parents who helped with a down payment, a paid-off used car gifted after college, and a small investment account that has been growing quietly since age 22. The other family has student debt, no family cushion, and a checking account that gets treated like an emergency room. Same salary range, wildly different lives.

The first household can take a career risk. They can move for a better opportunity, survive a bad quarter, put a kid in a better child care setup, or wait out a rough patch. The second household has to make safer decisions, not because they are less ambitious, but because a thinner margin for error punishes experimentation. When people say wealth creates freedom, this is what they mean. It buys the ability to recover.

Wealth inequality also affects time. A wealthier household can solve problems faster. Car trouble gets handled. Dental work gets scheduled. A broken laptop gets replaced before it becomes a work crisis. A renter facing a surprise fee may spend days rearranging bills, calling providers, and shifting payments. That is not just a money problem. That is a time-and-stress problem. Financial fragility consumes attention, and attention is a limited resource.

Then there is the emotional side. People with little wealth are often forced to make “smart” decisions that still feel like losing. Skip the vacation. Delay the move. Keep the older phone. Say no to the unpaid internship that might open doors later. Choose the safer college, the longer commute, the apartment with the worse school district. None of those choices looks dramatic from a distance. Together, they shape a life.

Wealth inequality also changes how childhood feels. In one home, a teenager’s problem is choosing among extracurriculars. In another, the teenager may already understand that one family illness, one rent hike, or one cut in work hours could rearrange everything. Kids notice more than adults think. They absorb whether the household feels buffered or brittle.

And as people age, the gap keeps talking. Wealthier families are better positioned to help adult children, weather layoffs, cover elder care, and retire with dignity. Families with thin assets often end up supporting both older and younger generations while still trying to stabilize themselves. That creates a kind of financial fatigue that no motivational quote can fix.

So when people ask, “How bad is wealth inequality in America?” the most accurate answer is not just that the top owns too much. It is that millions of Americans are living without enough margin for ordinary human mistakes, surprises, or ambitions. The wealth gap is not merely about luxury at the top. It is about vulnerability everywhere else.

Conclusion

So, how bad is wealth inequality in America? Bad enough that it shapes who gets security, who gets mobility, who gets to plan ahead, and who has to spend every month improvising. Bad enough that even when broad gains happen, the underlying structure still leaves vast differences in power and resilience. Bad enough that half the country can own only a sliver of total wealth while a tiny elite holds a massive share.

And perhaps most important, it is bad enough that the issue should no longer be treated like an abstract morality play about rich versus poor. It is an economic design problem. It influences health, education, housing, entrepreneurship, family stability, and retirement. In America, wealth inequality is not just about who lives best. It is about who gets to live with a margin of safety at all.