Table of Contents >> Show >> Hide

- Why Financial Advisor Costs Feel So Confusing

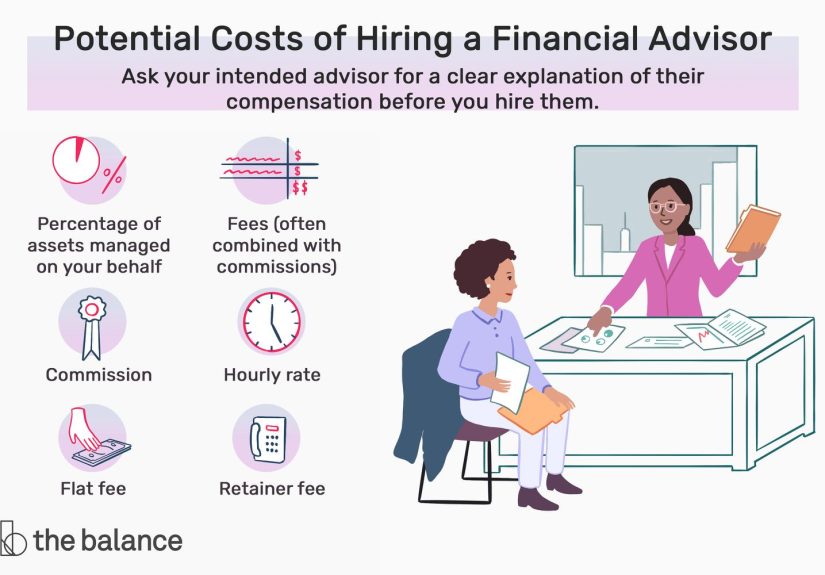

- The Main Ways Financial Advisors Get Paid

- What Those Fees Look Like in Real Dollars

- Robo-Advisors vs. Human Advisors: Cost Comparison

- What Drives the Cost of Advice Up or Down?

- Is a 1% Advisory Fee “Worth It”?

- How to Check and Compare Advisor Fees (Without Needing a PhD)

- Red Flags to Watch For in Advisor Pricing

- A Simple Checklist Before You Sign

- Real-Life Experiences With the Cost of Financial Advice

- Putting It All Together: Know Your Costs, Then Decide on Value

“How much does a financial advisor cost, really?” is one of the first questions people whisper

to Google right after, “Do I actually need one?” If you’ve ever wondered whether paying 1% of

your investments is normal, why some planners charge by the hour, or how robo-advisors stay so

cheap, you’re in the right place.

In this guide, we’ll unpack what you can realistically expect to pay for financial advice in

the United States, how the different fee models work, and how to decide whether the cost is

worth it for your situation. We’ll also walk through real-world examples, key questions to ask

before you sign an agreement, and what to do if you’re torn between a human advisor and a

lower-cost robo-advisor.

Why Financial Advisor Costs Feel So Confusing

Part of the confusion comes from the fact that there’s no single “menu price” for financial

advice. Advisors can charge a percentage of the money they manage for you, a flat annual fee,

an hourly rate, a one-time project fee, commissions on products they sell, or a combination of

all of the above.

Industry surveys generally show that:

- Traditional advisors often charge around 1% per year of assets under management (AUM).

- Flat annual retainers often range from about $2,500 to $9,000+.

- Hourly planning rates are usually in the $200–$400 per hour range.

- Robo-advisors commonly charge about 0.25% per year, sometimes less.

Those are broad averages, not price tags carved in stone. Your fee will depend on how much

money you have, the complexity of your finances, the services you’re getting, and how the

advisor structures their business.

The Main Ways Financial Advisors Get Paid

1. Assets Under Management (AUM) Fees

The percentage-of-assets model is still the industry’s go-to. Many fee-only and

fee-based advisors charge somewhere between 0.5% and 2% of the investments they manage,

with a “typical” fee right around 1% for many households. As your assets grow, the percentage

often drops in tiers (for example, 1% on the first $1 million, then 0.8% on the next chunk, and

so on).

A few quick examples:

- $100,000 managed at 1% = $1,000 per year.

- $500,000 managed at 1% = $5,000 per year.

- $1,000,000 managed at 0.9% blended rate = about $9,000 per year.

AUM fees are usually charged quarterly and pulled directly from your account, which makes them

feel almost invisibleuntil you do the math. Regulators and consumer sites routinely remind

investors that even a 1% annual fee can make a large difference in your long-term balance when

compounded over decades.

One nuance: some advisors bundle comprehensive financial planning (retirement projections,

tax strategies, estate planning, etc.) into that AUM fee; others charge extra for planning. If

you’re paying 1% and getting only investment selection and a yearly check-in, that’s very

different value than 1% plus robust planning and ongoing advice.

2. Flat Annual Retainers and Subscription Fees

Instead of tying fees to how much you’ve invested, some advisors charge a flat retainer or

a monthly subscription. Industry data often shows:

- Flat annual fees in the ballpark of $2,500 to $5,000+ for ongoing planning.

- Subscription models around $150 to $300 per month, depending on complexity.

This model can be attractive if:

- You have a solid income but not a huge investment account yet.

- You want comprehensive planning (student loans, stock options, insurance, taxes) more than just investment pick-and-choose.

- You like knowing the dollar amount you’ll pay each year, regardless of what the stock market does.

The key is to understand what’s included in that retainer: investment management, tax prep

coordination, estate planning guidance, regular meetings, email access, and so on.

3. Hourly Planning Fees

Hourly financial planning is the “pay as you go” version of advice. Surveys of advisors and

planning firms frequently show hourly rates clustered between $200 and $400, with some

advisors in higher-cost areas or with niche specialties charging more.

What might that look like in practice?

- 2–3 hours to review your situation and create a basic action list: maybe $600–$1,000.

- 8–10 hours for a full financial plan (retirement, debt payoff, insurance review): $1,600–$4,000.

Hourly advice is great if you:

- Prefer DIY investing but want a professional gut-check.

- Have a few specific questions (e.g., “Should I exercise my stock options this year?”).

- Don’t want an ongoing relationshipat least not yet.

4. One-Time Project or Per-Plan Fees

Some advisors charge a one-time project fee for creating a comprehensive written financial

plan. Reports from advisory firms commonly show these plans landing around the

$1,000–$3,000+ range, depending on the depth and complexity.

After that initial plan, you might:

- Implement it yourself, with no ongoing costs.

- Hire the advisor for hourly follow-ups.

- Transition into a retainer or AUM relationship so they help you keep the plan updated.

5. Commissions and Hybrid Models

Commission-based advisors earn money when you buy certain investment productslike mutual

funds, annuities, or insurance policiesthrough them. Industry comparisons often cite

commission ranges of about 3% to 6% of the transaction amount for some products.

That means a $10,000 investment with a 5% commission costs you $500 upfront, on top of any

ongoing fund or product expenses. Commission models can be appropriate in some contexts, but

they create potential conflicts of interest: the advisor earns more if you buy more, or buy

higher-commission products.

Many advisors today use a hybrid structureyou might pay an AUM fee for ongoing advice and

investment management, while the advisor also earns commissions on certain products (often

insurance). When that’s the case, it’s critical that you understand both streams of

compensation.

What Those Fees Look Like in Real Dollars

Percentages are nice, but dollars pay your bills. Let’s look at a simple comparison of AUM and

robo-advisor fees using the same portfolio.

Example: $250,000 Investment Portfolio

- Traditional advisor at 1% AUM: $2,500 per year.

- Traditional advisor at 0.75% AUM: $1,875 per year.

- Robo-advisor at 0.25%: $625 per year (plus underlying fund expenses).

Over 10 years, before factoring in investment growth or compounding:

- 1% advisor fee ≈ $25,000.

- 0.25% robo fee ≈ $6,250.

Regulators like the SEC regularly illustrate how even a small difference in annual fees

(say, 0.25% versus 1%) can significantly reduce your ending balance over a 20-year period.

Lower fees mean more of your returns stay in your accountbut only if you’re still getting the

guidance you actually need.

Robo-Advisors vs. Human Advisors: Cost Comparison

Robo-advisors are digital platforms that build and maintain a diversified portfolio for you

using algorithms. Many of the major names charge management fees around 0.25% per year,

sometimes as low as 0.05% for basic offerings, plus the underlying fund expenses.

On the cost side:

- Robo-advisors: roughly 0.05%–0.50% AUM in many cases.

- Human advisors: often around 1% AUM, sometimes more, sometimes less.

Many robo-advisors also offer automatic rebalancing, tax-loss harvesting, and goal-based

planning tools. Some are layering on access to human CFP® professionals for a higher fee tier,

which still often undercuts traditional advisory pricing.

So why would anyone pay 1% when 0.25% exists? The difference is usually scope and

human judgment. A robo-advisor can handle asset allocation and rebalancing very well. But it

won’t:

- Talk you down from panic-selling during a market crash.

- Help you decide when to claim Social Security.

- Coordinate tax strategies with your CPA.

- Design withdrawal strategies in retirement.

If your situation is straightforward and you’re comfortable with a digital interface, a

low-cost robo might be a smart move. If your finances are more complex (multiple accounts,

business ownership, equity comp, estate and tax planning), a human advisor may provide value

far beyond the feeassuming you pick the right one.

What Drives the Cost of Advice Up or Down?

Two people can walk into different advisors’ offices with the same account balance and get

very different quotes. Here are the biggest cost drivers:

1. Complexity of Your Situation

Someone with one 401(k) and a savings account is simpler to serve than a business owner with

multiple entities, rental properties, stock options, and legacy planning goals. Advisors often

charge more (or recommend higher-touch service tiers) when your situation is complex.

2. Services Included

Some firms focus primarily on investment management. Others offer a “family CFO” model with

deep tax collaboration, estate planning coordination, insurance analysis, and ongoing cash

flow coaching.

The more services wrapped into your fee, the more you should expect to payand the more value

you should demand in return.

3. Advisor Experience and Niche

Advisors with specialized expertise (for example, physicians, tech employees with stock

compensation, or business exit planning) may command higher fees. You’re not just paying for

their time, but for the years they’ve spent learning the quirks of situations like yours.

4. Firm Type and Location

Large national firms, boutique RIAs, and one-person shops all price differently. Advisors in

high-cost metropolitan areas often charge more than those in smaller cities or regions with

lower living expenses.

Is a 1% Advisory Fee “Worth It”?

The million-dollar (literally) question: is 1% too high, just right, or a bargain?

Research and industry commentary generally agree that around 1% AUM is common. The real

issue isn’t whether 1% is “good” or “bad” in a vacuumit’s what you’re getting for that money,

and whether you could reasonably get similar results at a lower cost.

A 1% fee looks much more reasonable if your advisor:

-

Keeps you invested through market volatility, preventing you from panic-selling in ways that

could cost far more than 1% in missed returns. -

Designs tax-efficient strategies that reduce your annual tax bill by hundreds or thousands of

dollars. - Optimizes your retirement timing and withdrawal strategy.

- Helps you avoid high-fee, poor-fit products.

On the other hand, if your advisor is essentially picking a few mutual funds once and doing

very little planning, communication, or behavioral coaching, then 1% may be expensive for what

you’re getting.

How to Check and Compare Advisor Fees (Without Needing a PhD)

Before you hire anyone, you should be able to answer three simple questions:

- How do you get paid?

- How much will I pay in dollars in the first year?

- What do I get for that fee?

Practical steps:

-

Ask for a clear fee schedule that shows AUM percentages, hourly rates, flat fees, and any

other charges. -

Request that the advisor show your fee in dollars based on your current portfolio (for

example, “With $400,000, you would pay $4,000 per year at 1%.”). -

Ask whether financial planning is included or billed separatelyand how many meetings and

check-ins you’ll get. -

Clarify whether they receive commissions on products and how that might influence their

recommendations. -

Review their regulatory filings (Form ADV, Part 2A) for a formal description of their fees,

conflicts of interest, and services.

Red Flags to Watch For in Advisor Pricing

Not all advisors are created equal. Pay attention to these warning signs:

- Vague answers about fees. If you feel like you’re playing “guess the price,” move on.

-

“Free” plans that are really product sales pitches. You might not pay upfront, but

you’ll pay through high-commission, high-expense products. -

High surrender charges or lock-ups. Products that make it expensive to leave can be a

problem, especially when you didn’t fully understand them going in. -

Pressure to move everything immediately. A good advisor can explain why changes make

sense, not rush you into a big rollover or product purchase.

A Simple Checklist Before You Sign

Before you commit to an advisor, run through this quick checklist:

- I know exactly how this advisor gets paid and at what rates.

- I’ve seen my estimated fee in dollars per year, based on my current situation.

- I understand what services are included and how often we’ll meet.

- I know whether the advisor is fee-only or can earn commissions.

- I’ve compared costs with at least one or two other advisors and/or robo-advisors.

- I feel comfortable asking questionsand I’ve gotten clear, jargon-free answers so far.

Real-Life Experiences With the Cost of Financial Advice

Numbers are helpful, but real-world stories show how fee structures feel in practice. Here are

a few composite experiences that mirror what many households encounter when they start

exploring financial advice.

Case 1: “We Thought 1% Was Too MuchUntil the Market Dropped”

Alex and Taylor had about $600,000 spread across 401(k)s, IRAs, and a taxable brokerage

account. They met with a fee-only advisor who quoted a 1% AUM feeroughly $6,000 per year. At

first, the number felt enormous. Their initial thought was, “We can just buy index funds

ourselves. Why would we pay someone $6,000 a year?”

They eventually decided to work with the advisor for a year and then reevaluate. Six months

later, the market went through a sharp downturn. Alex wanted to sell everything and “wait for

things to settle down.” Instead, their advisor walked them through their plan, their time

horizon, and the historical impact of panic-selling. They stayed invested, rebalanced, and

even used the downturn to harvest some tax losses in their taxable account.

A year later, their portfolio had recovered and then some. When they did the math, they

realized that avoiding a poorly timed sell-off probably saved them more than the 1% fee that

year. For them, the advisor’s behavioral coaching and tax work made the cost feel reasonable.

Case 2: “The Flat Fee Model Fit Our Growing Income, Not Our Small Portfolio”

Jordan and Priya were in their early 30s, earning strong six-figure incomes but with “only”

about $80,000 invested so far. A traditional 1% AUM model would have translated to roughly

$800 per year, but the advisors they interviewed weren’t very interested in clients with less

than $250,000 in assets.

They found a planner who charged a flat annual retainer of $3,000, payable monthly. That

sounded high compared to 1% on their current assets, but the advisor’s value proposition was

tailored to their reality: student loan strategies, cash-flow planning, tax-smart saving,

employee benefits, and a plan to buy their first home.

After a year, they could point to concrete changesautomatic savings set up, smarter equity

compensation decisions, a clearer investing plan, and a better handle on their monthly

spending. They felt like they were paying for judgment and guidance more than “just

investments,” which made the flat fee feel aligned with their stage of life.

Case 3: “We Started With a Robo, Then Upgraded to a Human”

Chris started with a robo-advisor charging 0.25% when they had about $25,000 invested. The

experience was simple: answer a few questions, get a diversified ETF portfolio, and let the

algorithm handle rebalancing. The annual feearound $62.50 at firstfelt like a bargain.

Over the next several years, Chris’s savings grew, and life got more complicated: a new job

with stock options, a partner with a different risk tolerance, and a desire to buy a home in a

high-cost city. The robo-advisor still managed the portfolio well, but it couldn’t answer

questions like, “Should I exercise these options when my company might go public?” or “How do

we structure our savings vs. down payment vs. retirement?”

Chris eventually hired a fee-only planner for a one-time project fee of about $2,500 to build

a comprehensive plan. They kept the robo for low-cost portfolio management but used the human

advisor’s plan as a roadmap. In their view, the robo fee remained a great deal for investment

execution, while the human advisor was worth the one-time cost for strategic decision-making.

Case 4: “We Walked Away From a ‘Free’ Plan That Wasn’t Really Free”

Another couple, Lisa and Miguel, attended a free retirement seminar at a local hotel. The

presenter offered complimentary retirement planning sessions. During their meeting, the advice

centered heavily on moving most of their retirement savings into high-commission annuities

with long surrender periods. The advisor insisted there were no upfront fees and emphasized

safety and guarantees.

After doing some homework, Lisa and Miguel realized that while they wouldn’t write a check

for the annuities, they would pay through embedded costs and limited flexibility. They backed

out and instead hired a fee-only planner for a project-based plan. The lesson: “free”

advice often has a priceyou just don’t see it itemized on an invoice.

Putting It All Together: Know Your Costs, Then Decide on Value

There’s no universally “correct” way to pay for financial advice. A 0.25% robo-advisor can be

perfect for one investor, while a 1% full-service planner is a bargain for someone with a more

complex life and higher stakes decisions.

What matters most is clarity. You should know:

- How your advisor charges (AUM, flat, hourly, commissions, or hybrid).

- What you’ll pay in dollars each year.

- Exactly what services you get in return.

Once you understand those pieces, you’re not just “hoping” a financial advisor is worth the

costyou’re making an informed, confident decision about how much you’re willing to pay for

expert guidance on your money.