Table of Contents >> Show >> Hide

- First, a quick translation: “fund” vs. “account”

- Why this fund matters more than ever in 2026

- The big idea: a target-date fund is a retirement portfolio on autopilot

- The “most important” part: fund it up to the match, then invest it sanely

- How to choose the right target-date fund in your plan

- A concrete example: how the “most important fund” plays out

- Common mistakes that quietly wreck retirement progress

- But what about Roth vs. traditional? (Yes, it matters. No, it shouldn’t paralyze you.)

- Quick-start checklist: get your “most important retirement fund” working this week

- Conclusion: the most important retirement fund is the one you’ll actually fund

- Real-world experiences: what this looks like in practice (and what people learn)

If you were hoping for a single, magical ticker symbol that turns your future self into a beach-dwelling

millionaire with suspiciously perfect hair… I have both good news and boring news. The good news: there

is a “most important retirement fund” for most people right now. The boring news: it’s usually not

a secret hedge fund run by a guy named Chip.

For the majority of American workers, the most important retirement fund right now is a

low-cost target-date retirement fund inside your workplace 401(k) (or similar plan)funded

at least up to the full employer match. That combination is the closest thing personal finance

has to a cheat code: diversified investing + automation + (often) free money.

This article explains why target-date funds (TDFs) in employer plans matter so much in 2026, how to pick a

good one, what mistakes to avoid, and when you should prioritize other accounts like a Roth IRA or an HSA.

(Spoiler: your money can have more than one best friend.)

First, a quick translation: “fund” vs. “account”

People say “retirement fund” to mean two different things:

- The account: 401(k), 403(b), IRA, Roth IRA, HSA, etc. (This is the container.)

- The investment fund: target-date fund, S&P 500 index fund, bond fund, etc. (This is what you buy inside the container.)

The reason target-date funds win the “most important” trophy for so many people is that they solve both

problems at once: they’re designed specifically for retirement, and they’re usually the simplest high-quality

choice inside a 401(k).

Why this fund matters more than ever in 2026

1) The employer match is still the most underappreciated raise in America

A 401(k) match is one of the only places in modern life where “free money” is a real thing and not a scammy

email from a “Nigerian prince.” Contribute enough, and your employer adds money too. Miss the match, and

you are essentially saying, “No thanks, I’m good” to part of your compensation.

Example: if your employer matches 50% of what you contribute up to 6% of your pay, contributing 6% could

produce a 3% matchevery paycheck. That’s an immediate, risk-free return on your contribution before the

market even shows up to work.

2) Contribution limits rosemeaning you can shelter more income

The IRS increased several retirement-related limits for 2026, which matters because the easiest way to build

a strong retirement is to consistently invest meaningful amounts in tax-advantaged accounts:

- 401(k)/403(b)/governmental 457/TSP employee limit (2026): $24,500 (plus catch-up contributions if eligible).

- 401(k) catch-up (age 50+ in 2026): $8,000; higher “super catch-up” applies for ages 60–63 in many plans.

- IRA contribution limit (2026): $7,500; catch-up for age 50+ is $1,100 (so $8,600 total).

- HSA contribution limit (2026): $4,400 self-only or $8,750 family (plus $1,000 catch-up at age 55+ if eligible).

These numbers aren’t triviathey’re capacity. If you’ve been saving “whatever is left,” 2026 is a strong

year to flip the script: decide what you want to save first, then let your spending adapt like a reality show

contestant who just realized the cameras are rolling.

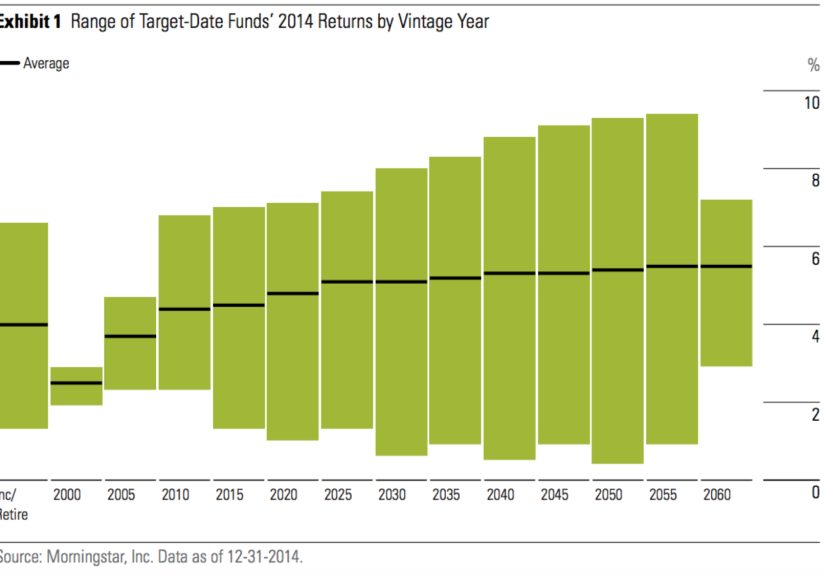

The big idea: a target-date fund is a retirement portfolio on autopilot

A target-date retirement fund typically holds a diversified mix of stock and bond funds that automatically

becomes more conservative as you approach the fund’s target year (often the year you’ll turn about 65).

It rebalances for you, meaning it regularly nudges your portfolio back toward its intended allocation

without you needing to babysit it.

What makes target-date funds so effective for most people

- Instant diversification: U.S. stocks, international stocks, bondsoften in one fund.

- Automatic rebalancing: You don’t have to remember to do it (or pretend you will).

- Age-based risk management: The fund’s “glide path” gradually reduces risk over time.

- Behavioral advantages: A simple default can help you stay invested through market drama.

When target-date funds can be a bad fit

Target-date funds aren’t perfect. They can be a poor choice if:

- Fees are high: Some are inexpensive index-based funds; others are pricier and actively managed. Fees matter.

- Your plan offers a weak lineup: Some plans have “target-date” in the name but underdeliver in diversification or cost.

- You hold a TDF in a taxable brokerage account: It can create tax surprises. (TDFs are usually best in retirement accounts.)

- Your retirement plan is unusual: A pension, early retirement plans, or extreme risk preferences may call for customization.

Still, for most peopleespecially anyone who wants a high-quality “set it and keep living your life”

approacha low-cost target-date fund in a workplace plan is an A-grade solution.

The “most important” part: fund it up to the match, then invest it sanely

Your two biggest levers in retirement investing are:

(1) how much you contribute and (2) whether you stay invested.

A matched 401(k) contribution into a target-date fund helps with both.

A simple retirement saving “order of operations” (for many households)

-

401(k) to the full match

Put your contributions into a low-cost target-date fund (or a low-cost diversified index option if you know what you’re doing). -

HSA (if eligible) as a “stealth retirement account”

If you can afford to pay current medical costs out of pocket, investing HSA funds for the long run can be powerful because qualified medical withdrawals are tax-free. -

Roth IRA (if eligible) or Traditional IRA (if it makes sense)

Great for flexibility and (in Roth’s case) tax-free qualified withdrawals in retirement. -

Back to the 401(k) toward your target savings rate

Many planners use 15% of income (including match) as a starting point, then adjust based on goals. -

Taxable brokerage for extra goals

More flexibility, fewer tax advantages, still very useful.

Your “right” order can change based on your income, debt, cash-flow needs, and whether you’re eligible for

certain accounts. But in general, getting the match is hard to beat.

How to choose the right target-date fund in your plan

Step 1: Pick the target year based on your likely retirement window

Most target-date funds are labeled with a year (e.g., 2055, 2060). A common approach is to pick the year

you’ll turn about 65. If you plan to retire earlier, you might choose an earlier date; if later, a later date.

The year is less about destiny and more about how aggressively the fund invests over time.

Step 2: Look for low costs (the unsexy superpower)

In plain English: if two funds do roughly the same job, the cheaper one gives you better odds. In a 401(k),

this usually shows up as the fund’s expense ratio. Many plans have both “index” and “active” target-date

seriesindex series are often (not always) cheaper.

Step 3: Understand the glide path (aka how the fund “grows up”)

Target-date funds differ in how quickly they reduce stock exposure. Some stay more stock-heavy longer;

others get conservative earlier. Neither is universally “best”but you should know what you’re buying so you

don’t panic-sell when the market has one of its legendary tantrums.

Step 4: Avoid accidental duplication

If you use a target-date fund as your core, you usually don’t need to add a bunch of extra stock and bond

funds “for balance.” A target-date fund is already balanced. Adding more funds can make your portfolio

lopsided, like putting extra toppings on pizza until it becomes a casserole.

A concrete example: how the “most important fund” plays out

Meet Sara, 32, earning $80,000. Her employer matches 50% up to 6% of pay. She chooses a low-cost target-date

fund in her 401(k).

- Sara contributes 6%: $4,800/year.

- Employer match (50% of 6%): $2,400/year.

- Total added to retirement: $7,200/year.

That match is a built-in boost. Over a long career, consistent contributions plus market growth can compound

dramatically. The exact ending balance depends on returns, fees, and timebut the match raises Sara’s savings

rate without requiring her to “feel” the full amount in her paycheck.

Now Sara levels up: she increases her contribution by 1% each year until she’s saving 12–15% (including match).

It’s a strategy that often feels manageable because it rides along with raises instead of fighting them.

Common mistakes that quietly wreck retirement progress

1) Missing the match (the classic “free money left on the table” move)

If your budget is tight, it’s tempting to contribute “later.” But if you can contribute even enough to get the

match, you’re effectively turning part of your paycheck into an immediate return.

2) Accidentally maxing too early and losing match per paycheck

Some plans match each paycheck. If you front-load contributions and hit the annual limit early, you might miss

match on later paychecks unless your plan offers a “true-up” match. If you’re a high saver, check how your plan

handles this so you don’t sabotage yourself with enthusiasm.

3) Paying high fees without realizing it

Fees are like a leak in your financial boat: small at first, then mysteriously you’re paddling. If your plan’s

target-date funds are expensive, you might do better building a simple portfolio from low-cost index funds

(e.g., total U.S. stock + international stock + bond), or using the cheapest diversified option available.

4) Treating a target-date fund like a trading account

Target-date funds work best when you let them do their job. The goal is not to outsmart the market weekly.

The goal is to retire without needing to host a bake sale at 78.

But what about Roth vs. traditional? (Yes, it matters. No, it shouldn’t paralyze you.)

Traditional 401(k) contributions generally reduce taxable income now, and you pay taxes when you withdraw in

retirement. Roth 401(k) contributions are after-tax now, and qualified withdrawals can be tax-free later.

Many savers benefit from having both types over time for tax flexibility.

A simple heuristic:

- If you’re early in your career or currently in a lower tax bracket: Roth contributions may be appealing.

- If you’re in peak earning years and facing high marginal tax rates: Traditional contributions can be powerful.

- If you’re unsure: split contributions between Roth and traditional, or prioritize the match first and refine later.

The most important thing is consistency. Tax strategy helps; savings rate and staying invested help more.

Quick-start checklist: get your “most important retirement fund” working this week

- Find your match formula (HR portal, benefits guide, or plan website).

- Set your contribution to capture the full match (start here, then increase gradually).

- Select a low-cost target-date fund close to your retirement year (or the best diversified option available).

- Turn on automatic escalation if your plan offers it (1% per year is a popular “pain-minimizing” setting).

- Check your beneficiaries (this is the most ignored, most important paperwork in adult life).

- Review once a yearnot daily. Your retirement account is not a reality TV show.

Conclusion: the most important retirement fund is the one you’ll actually fund

In 2026, the “most important retirement fund right now” for most Americans is a

low-cost target-date fund inside a matched 401(k). It’s diversified, automatically adjusted over time,

and paired with one of the strongest incentives available: the employer match.

If you do nothing else, do this: contribute enough to get the full match, pick a solid target-date fund, and keep

showing up. Retirement isn’t built by perfect decisions. It’s built by repeated, slightly boring ones.

Real-world experiences: what this looks like in practice (and what people learn)

Below are three common “I wish someone told me sooner” experiences that show up again and again in real

households. If you recognize yourself, congratulationsyou’re a normal human, not a financial robot.

Experience #1: The Match Wake-Up Call

A lot of people start out contributing 1–2% to a 401(k) because it feels responsible and minimally painful.

Then they discover their employer matches up to 4–6% and realize they’ve been skipping a benefit that’s

basically part of their pay. The emotional reaction is usually a mix of “Wait, WHAT?” and “Please don’t tell

my past self.” Once they bump contributions up to the match, something interesting happens: they adapt.

They spend a little less, complain for two weeks, then forget it ever happenedwhile their retirement

balance starts growing faster.

The biggest lesson from this experience is behavioral: people don’t fail because they hate retirement. They

fail because the steps aren’t obvious and the default is inaction. A target-date fund helps because it reduces

the number of choices you have to get right. You don’t need to become an expert in small-cap value versus

international developed markets. You just need to pick the date and keep feeding the machine.

Experience #2: The “I Thought My Money Was Invested” Surprise

This one is painfully common: someone enrolls in the 401(k), contributions start, and they assume the plan

automatically invests the money. Months (or years) later they check the account and discover it’s sitting in a

cash-like default option with tiny returns. Cue the “I have been betrayed by adulthood” feeling.

The fix is simple and takes five minutes: choose the target-date fund (or another diversified option), confirm

your future contributions go there, and check whether existing cash needs to be moved. The lesson is also

simple: retirement investing rewards small setup tasks. The difference between “contributing” and “contributing

and investing” is the difference between buying groceries and actually cooking.

Experience #3: The HSA Becomes a Retirement Power Tool

People often treat an HSA like a fancy checking account for copays. Then they learn it can be invested, rolls

over year to year, and offers unique tax advantages for qualified medical expenses. A common “level up” strategy

is: contribute to the HSA, invest it, and pay current medical expenses out of pocket if affordablesaving receipts

in case they want to reimburse themselves later. Over time, the HSA can become a dedicated “healthcare in

retirement” fund, which matters because healthcare is one of the biggest expenses many retirees face.

The lesson: the “most important retirement fund” is sometimes a team sport. For many savers, the 401(k)

target-date fund is the foundation (especially with the match), the Roth IRA adds flexibility and tax-free income,

and the HSA helps cover future healthcare costs. You don’t need to max everything immediately. Start with the

match, automate increases, and build the rest in layerslike a smart financial lasagna.