Table of Contents >> Show >> Hide

- First, what does “return” even mean for mortgage prepayments?

- Why mortgage math confuses people (and why that matters)

- The “return” you get: a simple way to estimate it

- Let’s do real math with a realistic example

- So why do people say the return can be “less than your mortgage rate”?

- The timeline problem: your “return” depends on how long you keep the mortgage

- When mortgage prepayments look especially smart

- When investing may beat prepaying (even if prepaying feels better)

- Gotchas that can quietly wreck the “return”

- A simple framework for deciding (no spreadsheets required… unless you enjoy them)

- Bottom line: what’s the return on mortgage prepayments?

- Real-World Experiences With Mortgage Prepayments (Common Scenarios)

- 1) “My rate is 6%+ and I’m tired of the payment.”

- 2) “I have a low-rate mortgage, but I hate debt.”

- 3) “I got a bonus/inheritance and I want to ‘do something responsible.’”

- 4) “We’re planning for kids/college/retirement and want the mortgage gone by a deadline.”

- 5) “We prepaid aggressively… then moved sooner than expected.”

- 6) “Paying extra felt amazing… until we realized we weren’t investing at all.”

Paying extra on your mortgage feels like the most “adulting” financial move ever. You picture your future self sipping coffee, mortgage-free,

financially serene, possibly wearing linen. But then a very annoying question shows up:

What’s the return on mortgage prepayments?

Is it basically the same as your mortgage rate (a sweet, “guaranteed” win)? Or is it lower, because mortgage math has a way of turning confident

people into googling goblins at 1:00 a.m.?

Let’s unpack the real returnfinancially and emotionallyusing plain-English math, realistic scenarios, and a few “wait… what?” gotchas that

matter in real life.

First, what does “return” even mean for mortgage prepayments?

When you invest in a stock or fund, your return is what you earn. When you prepay a mortgage, your “return” is what you

avoid paying: future interest.

That makes mortgage prepayments a little different from investing:

- It’s closer to a guaranteed return (because it’s based on your loan contract).

- It’s usually not liquid (your money moves into home equity, not a savings account).

- It can be time-dependent (moving or refinancing changes how much of the benefit you actually keep).

The cleanest way to think about it is:

Mortgage prepayments can earn a “return” roughly equal to your mortgage’s effective interest rateadjusted for taxes and

your timeline.

Why mortgage math confuses people (and why that matters)

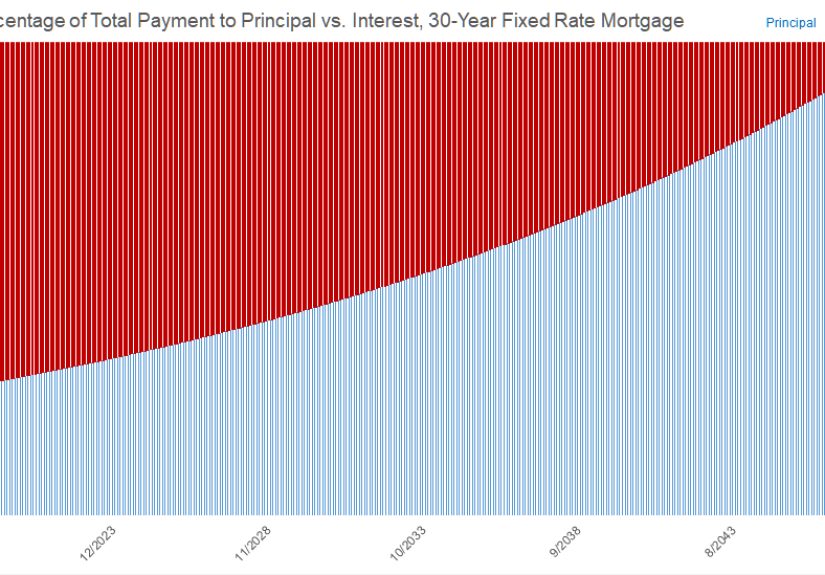

1) Amortization front-loads interest

Most fixed-rate mortgages are amortized: you make the same payment each month, but the split between interest and principal changes over time.

Early on, the interest portion is bigger because your loan balance is bigger. Over time, as the balance shrinks, interest shrinks too.

This is why people love the idea of prepaying: extra money goes straight to principal, which lowers the balance, which reduces future interest.

You’re basically shrinking the “interest engine” inside your mortgage.

2) Interest is calculated on what you still owe

Mortgage interest is based on your outstanding principal balance. Reduce the balance, and you reduce the interest that accrues going forward.

That’s the fundamental reason prepayments work.

Practical takeaway: an extra principal payment saves interest immediatelystarting with your very next interest calculation.

The “return” you get: a simple way to estimate it

Here’s a quick-and-useful rule of thumb:

Approximate annual return on extra principal ≈ your mortgage rate (after taxes).

Why “after taxes”? Because taxes can change the effective cost of your mortgage and the effective benefit of alternatives (like a high-yield

savings account or Treasury bills).

Step 1: Find your effective mortgage rate

If you do not itemize deductions, your effective mortgage rate is basically your note rate.

If you do itemize, the mortgage interest deduction can reduce the effective cost of your mortgage (subject to limits and your

situation). That means the “return” on prepaying may be lower than the stated rate because some of the interest you pay would have been

tax-deductible anyway.

A rough estimate:

Effective mortgage rate ≈ Mortgage rate × (1 − marginal tax rate) (only on the deductible portion, only if itemizing)

This is one reason the “return” isn’t one-size-fits-alltwo households with the same mortgage rate can have different after-tax results.

Step 2: Compare it to your alternatives (also after tax)

Your realistic alternatives usually include:

- High-yield savings / money market (taxable interest)

- Treasuries (federal taxable; often state tax advantages)

- Index funds / retirement accounts (higher expected return, but not guaranteed)

- Paying other debt (often higher rates than mortgages)

The mortgage prepayment return is “safe,” but it may or may not be the best use of your next dollar depending on your rate, risk tolerance,

and goals.

Let’s do real math with a realistic example

Assume a $300,000 30-year fixed mortgage at 6.15%. (This is in the neighborhood of recent U.S. 30-year fixed

averages, just to keep things grounded in reality.)

Baseline: pay it normally

- Monthly principal & interest: about $1,828

- Total interest over 30 years: about $358,000

- Total paid over 30 years: about $658,000

Yes, the interest is roughly “another house.” No, you’re not being dramatic for feeling attacked by that.

Option A: Add the equivalent of one extra payment per year

One simple strategy is to pay an extra amount monthly equal to one full payment spread over 12 months. Here, that’s about

$152/month.

- New payoff time: ~24.5 years (about 5.5 years sooner)

- Interest saved: ~ $77,500

That’s not a flashy crypto moonshot. But it’s meaningful, guaranteed, and gets you out of the mortgage business years earlier.

Option B: Make a $30,000 lump-sum prepayment early on

If you drop $30,000 on principal and keep your normal payment (typical setup), you shorten your loan dramatically.

- New payoff time: ~23.1 years

- Total savings vs baseline: ~ $120,000+ (mostly interest you never pay)

Now, what’s the “return” on that $30,000?

In the simplest sense, that extra $30,000 reduces interest immediately.

The first-month interest savings alone are roughly:

$30,000 × 6.15% ÷ 12 ≈ $154

Annualized, that’s basically your mortgage ratebecause the “earnings” are the interest you don’t pay.

Over time, as the loan balance drops faster, the savings accumulate.

So why do people say the return can be “less than your mortgage rate”?

You’ll sometimes hear an argument like: “If your extra payment knocks out payments near the end of the loan, those payments have less interest,

so the return is small.” It sounds reasonable… and it can be misleading depending on what you’re actually measuring.

Here’s the clearer version:

- If your extra payment truly reduces principal, you save interest based on your rate, starting immediately.

-

If your “extra payment” is treated as paying ahead (not reducing principal), you may not get the interest savings you expect.

This is why it matters to ensure the lender applies it correctly. -

If you move or refinance earlier than expected, you might not keep the full long-term benefitbecause you won’t be holding the

mortgage long enough for the “skipped later payments” to actually happen.

In other words, the mortgage rate is the starting point, but your timeline and execution determine the final

“return.”

The timeline problem: your “return” depends on how long you keep the mortgage

If you’re likely to sell the home or refinance in, say, 3–7 years, the return calculation becomes more practical:

you only benefit from the interest you avoid during the years you actually have the loan.

That doesn’t mean prepaying is uselessit just means you should evaluate prepayments like a decision with a time horizon.

Paying down a mortgage you won’t keep for long can be like buying a 30-year bond and selling it a few years later: you may get some benefit,

but not the full intended ride.

When mortgage prepayments look especially smart

1) Your rate is high

The higher your mortgage rate, the higher the guaranteed “return” from prepayingagain, adjusted for taxes.

At rates around 6%+, prepayments can compete with many low-risk alternatives.

2) You’re building financial flexibility (especially near retirement)

A paid-off home reduces your required monthly spending. That can matter more than squeezing out the last decimal of expected investment return.

Cash-flow freedom is underrated until you’re staring at a market dip and a fixed mortgage payment at the same time.

3) You value certainty and sleep

A mortgage prepayment is like a “guaranteed return” that doesn’t email you daily volatility updates.

If you know you won’t consistently invest the difference, prepaying can function as forced savingsand forced savings beats theoretical genius.

When investing may beat prepaying (even if prepaying feels better)

1) Your mortgage rate is low

If you locked a 2.75%–3.50% mortgage in the low-rate era, your “return” on prepaying is also low.

In that case, long-term investing (especially in tax-advantaged accounts) can have a stronger expected payoffthough not guaranteed.

2) You’re leaving “free money” on the table

If you have an employer retirement match and you’re not capturing it, that’s often a higher-impact move than prepaying a mortgage.

A match can be an immediate return that mortgage math simply can’t compete with.

3) Liquidity matters to you right now

Extra payments tie cash up in home equity. Accessing it later usually requires refinancing, a HELOC, or sellingnone of which are guaranteed,

cheap, or convenient at the exact moment you’d like them to be.

Gotchas that can quietly wreck the “return”

1) Prepayment penalties (rare, but real)

Many mortgages do not have prepayment penalties, but some loans can. If your loan has a penalty and you prepay aggressively, the penalty can

reduce (or wipe out) the benefitespecially if you plan to refinance or sell early.

Always check your loan documents or call your servicer before making a large prepayment.

2) Make sure extra payments go to principal

When you make an extra payment, specify that it should be applied to principal.

Some systems default to “paying ahead,” which may not reduce interest the way you expect.

3) Taxes are personal (and the deduction isn’t universal)

A mortgage interest deduction can reduce the effective cost of borrowingbut only if you itemize, and only within the applicable limits.

Since many households take the standard deduction, the practical tax benefit may be smaller than people assume.

4) Recasting vs. just paying extra

A recast (when allowed) keeps your rate and term but reduces your monthly payment after a lump-sum principal reduction.

The financial “return” still comes from reduced interest, but the lifestyle benefit is improved cash flow.

This can be a great middle ground if you want breathing room without refinancing.

A simple framework for deciding (no spreadsheets required… unless you enjoy them)

Use this checklist

- Do you have an emergency fund? If not, build that first. A paid-off mortgage is great; a surprise expense with no cash is not.

- Is your mortgage rate high (around 6%+)? Prepaying becomes very competitive.

- Are you maxing any “high-return” basics? Employer match, high-interest debt payoff, and necessary insurance usually come before extra mortgage payments.

- Will you stay in the home long enough? If you’re likely to move or refinance soon, focus on the payoff horizon you’ll actually experience.

- Do you crave certainty? If peace of mind is the goal, prepaying can be “worth it” even if investing might win on paper.

Bottom line: what’s the return on mortgage prepayments?

In most typical cases where extra payments truly reduce principal, the financial “return” on mortgage prepayments is

roughly your mortgage’s effective interest rateadjusted for taxes and your holding period.

But the decision isn’t only math. It’s also:

- your need for liquidity,

- your time horizon,

- your comfort with market risk, and

- the emotional “return” of owning your home free and clear.

If you want the most “common sense” answer: optimize the big wins first (emergency fund, high-interest debt, retirement match),

then decide whether extra mortgage payments fit your goals and your personality. Your spreadsheet doesn’t have to live your life. You do.

Real-World Experiences With Mortgage Prepayments (Common Scenarios)

You don’t need a finance degree to notice a pattern: people don’t decide to prepay mortgages because they’re bored.

They do it because something in real life makes “guaranteed savings” feel more valuable than “possible gains.”

Below are common experiences homeowners talk about when they’re weighing the return on mortgage prepayments. These aren’t personal stories from

mejust realistic, frequently seen situations that show how the math and the emotions collide in the wild.

1) “My rate is 6%+ and I’m tired of the payment.”

When mortgage rates are high, the appeal is obvious: extra principal can act like a solid, contract-backed return. Many people in this camp

treat prepayments as their “safe bucket.” They’re still investing for the long term, but they use prepayment as a way to reduce monthly pressure.

The most common shift is psychological: they go from feeling like the mortgage is a permanent roommate to feeling like it’s a countdown timer.

2) “I have a low-rate mortgage, but I hate debt.”

This is the classic head-versus-heart scenario. The spreadsheet might whisper, “Invest the difference,” especially if the mortgage rate is

3% or less. But plenty of homeowners still prepay because the emotional return is massive. They describe it as “quieting the noise.”

And here’s the key: if someone is unlikely to invest consistently, then prepaying isn’t just emotionalit can be strategically realistic.

The best plan is the plan you’ll actually follow.

3) “I got a bonus/inheritance and I want to ‘do something responsible.’”

Lump sums trigger decision paralysis. Investing feels risky, spending feels irresponsible, and leaving it in cash feels like doing nothing.

Prepaying often becomes the “responsible default.” The experience that follows depends on liquidity needs. People who keep a healthy cash buffer

tend to feel great about the decision. People who throw every spare dollar at the mortgage sometimes regret it when an unexpected expense pops up

and the only way to access cash is borrowing again at today’s rates.

4) “We’re planning for kids/college/retirement and want the mortgage gone by a deadline.”

Deadline-driven prepayment is extremely common. The goal isn’t necessarily maximizing net worth; it’s maximizing options. Parents often want the

mortgage gone before tuition hits, and retirees often want fixed expenses lower before leaving the workforce. In these situations, the “return”

includes flexibility: fewer required payments means a smaller monthly nut, which can reduce stress during market downturns or income changes.

5) “We prepaid aggressively… then moved sooner than expected.”

This is where timeline risk becomes real. People prepay thinking they’ll stay 15–30 years, then life happens: a job relocation, family needs,

or simply a desire for a different home. The good news is that extra principal typically becomes equity, so it’s not “lost.”

The less-good news is that the full interest-saving journey might not play out as plannedespecially if a refinance or sale happens quickly.

The lesson most people take from this: if you might move soon, keep flexibility higher and treat prepayment as a smaller, optional levernot a

full-time obsession.

6) “Paying extra felt amazing… until we realized we weren’t investing at all.”

A surprisingly common experience is “accidental under-investing.” Homeowners feel proud seeing the mortgage balance drop fast, but later realize

they missed years of retirement contributions. The most balanced households tend to adopt a two-lane approach: automatic investing (so it

actually happens) and then extra mortgage payments with whatever remains. That structure keeps the emotional benefits of prepaying while still

preserving long-term wealth building.

The big takeaway from these real-world scenarios is that the “return” on mortgage prepayments isn’t just a number. It’s a blend of contract-backed

savings, your personal risk tolerance, your timeline, and how much you value freedom from a required monthly payment. The best decision is usually

the one that improves your financial stability and your behaviorbecause math is powerful, but habits are undefeated.