Table of Contents >> Show >> Hide

- Inflation 101: The Return You Get vs. the Return You Keep

- How Inflation Pushes Markets Around: Three Big Channels

- Stocks and Inflation: Not a Simple Love Story (More Like a Complicated Situationship)

- Bonds and Inflation: Why “Fixed Income” Sometimes Feels Like “Fixed Disappointment”

- So What Happens to “Market Returns” When Inflation Changes?

- A Real-World Snapshot: When Inflation Spiked, Markets Repriced Fast

- Common-Sense Moves to Deal with Inflation (Without Panicking)

- Bottom Line: Inflation Changes the Game, Not the Goal

- Experiences: What Inflation Feels Like in Real Portfolios (And What People Learn)

- SEO Tags

Inflation is the financial equivalent of a slow leak in your tire. You can still drive for a while, but eventually you’ll wonder why your portfolio feels “fine”

while your grocery bill looks like it’s training for the Olympics.

The tricky part: inflation doesn’t just change what things cost. It changes how markets price risk, how central banks set interest rates, how investors behave,

andmost importantlywhether your returns are actually building wealth or just keeping up with a more expensive world.

This is the “wealth of common sense” version of the story: inflation matters, but not in a simple “inflation up, stocks down” way. The relationship is messy,

nonlinear, and full of context. That’s annoying. But it’s also usefulbecause it means you’re not doomed every time the CPI prints a spicy number.

Inflation 101: The Return You Get vs. the Return You Keep

Most market returns you see quoted are nominal returnsreturns measured in dollars, without adjusting for inflation. What you actually care about

is your real return: how much your purchasing power grew after prices rose.

The quick math (aka “don’t let your brain do the rounding”)

A simple estimate is: real return ≈ nominal return − inflation. That’s fine for back-of-the-napkin thinking.

But if you want the more accurate version:

Real return = (1 + nominal return) / (1 + inflation) − 1

Example: if your portfolio gains 8% and inflation is 3%, your real return is roughly:

(1.08 / 1.03) − 1 ≈ 4.85%. That’s still goodbut it’s not 8%. Inflation just quietly took a tip.

This is why inflation can create a “money illusion”: you feel richer because the number went up, even if what that number buys didn’t improve much.

Your portfolio didn’t lie to youyour measuring tape did.

How Inflation Pushes Markets Around: Three Big Channels

1) Interest rates and discount rates (the valuation thermostat)

When inflation rises, interest rates often rise tooeither because the central bank is trying to cool demand, or because lenders want compensation for

losing purchasing power over time. Higher rates don’t just affect mortgages; they change how markets value future cash flows.

Think of stocks as a stream of future profits. When the “discount rate” rises, those distant future dollars are worth less today. This tends to pressure

high-growth companies whose value is more dependent on far-off earnings. It can also compress price-to-earnings (P/E) multiples across the market.

2) Corporate fundamentals (pricing power vs. cost pressure)

Inflation can be friendly or hostile depending on whether companies can raise prices without losing customers. Businesses with strong brands, essential products,

or scarce assets may pass along costs. Others get squeezed: wages, materials, shipping, and borrowing costs rise faster than revenue, and margins take the hit.

3) Uncertainty and sentiment (the vibes channel, but make it expensive)

High or volatile inflation often comes with “everything feels unstable” energy: changing policy, shifting consumer behavior, and unpredictable input costs.

Markets hate uncertainty almost as much as they hate paying full price.

That doesn’t mean stocks can’t do well during inflationary periods. It means the ride can get bumpier, and the winners and losers can rotate in surprising ways.

Stocks and Inflation: Not a Simple Love Story (More Like a Complicated Situationship)

The most common myth is: “Inflation is always bad for stocks.” The more accurate statement is:

extreme inflation tends to be bad for markets, but moderate inflation often coexists with decent returns.

That “nonlinear” relationship is a key idea discussed in A Wealth of Common Sense: inflation at very low or very high levels can be associated with weaker

market outcomes, while “normal-ish” inflation often comes with a functioning economy, growing wages, and improving corporate revenues.

Why moderate inflation isn’t automatically terrible

Stocks represent ownership of real businesses. Real businesses can raise prices, innovate, replace products, and adapt. Over long horizons, equities have

historically been one of the better tools for staying ahead of inflationnot because they’re immune, but because they’re alive.

If the overall economy is growing and inflation is steady (not chaotic), companies can often maintain profitability. In that environment, nominal revenue growth

can look strong, and the market can keep moving higher.

Why high inflation can hurt stocks (especially in the short run)

High inflation can force rapid policy tightening, which raises borrowing costs, cools demand, and can increase recession risk. If profits fall while rates rise,

you get the double-whammy: earnings pressure and valuation compression.

This is why “inflation fears” often show up as volatility spikes. The market isn’t scared of higher prices in a vacuumit’s scared of what higher prices

might make policymakers do, and what that might do to growth.

Value vs. growth when inflation changes

A Wealth of Common Sense has also noted a pattern many investors have felt in their bones: when inflation runs higher, value stocks (companies

priced more on current cash flows) have often held up better than long-duration growth stocks (priced more on future expectations).

It’s not a law of physics. It’s a tendency. But it lines up with the discount-rate story: when rates rise, “future dollars” get discounted harder.

Dividends help, but they’re not a force field

Dividends can soften the blow in inflationary periods because a portion of your return is paid out now (instead of promised later). But dividends don’t

automatically beat inflation. What matters is whether the underlying business can grow earnings and raise dividends over time.

Bonds and Inflation: Why “Fixed Income” Sometimes Feels Like “Fixed Disappointment”

Bonds are simple on paper: you lend money, you get interest, you get your principal back. Inflation makes that simplicity… emotionally complicated.

Inflation erodes purchasing power

If you own a bond paying 4% and inflation is 3%, your real return is about 1% before taxes. If inflation is 5%, you’re effectively running on a treadmill

that’s speeding up while you’re holding a cup of water. Spill risk increases.

Why bond prices fall when rates rise

When new bonds are issued at higher yields, older bonds with lower coupons become less attractiveso their prices fall. The longer the maturity (and the

longer the “duration”), the more sensitive the bond price is to rate changes.

That’s why inflation surprises can hit bonds hard: markets may reprice expected inflation and expected policy rates quickly, and longer-duration bonds can feel it

like whiplash.

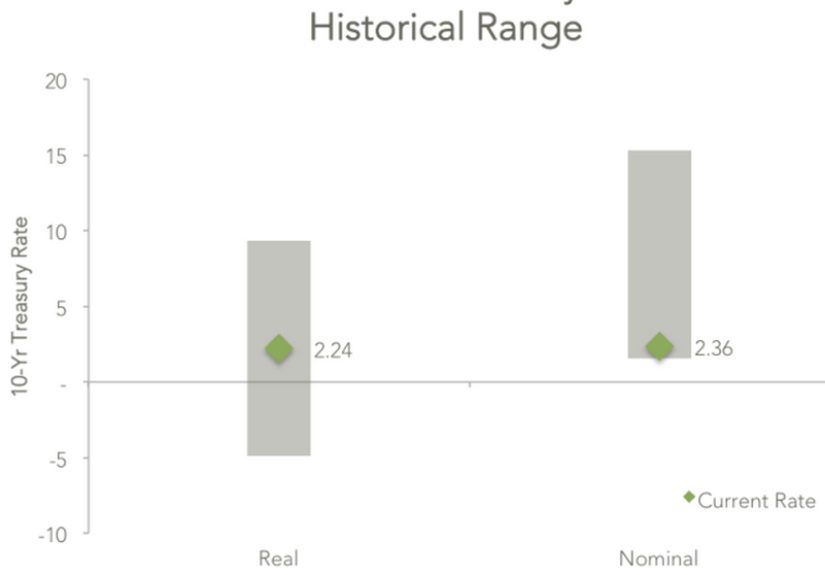

TIPS: A bond designed to fight inflation (with a few caveats)

Treasury Inflation-Protected Securities (TIPS) adjust their principal based on inflation (as measured by CPI). When inflation rises,

the principal value rises, and interest paymentscalculated off that principalrise too.

Important nuance: TIPS can still fluctuate in price before maturity because real yields change. But held to maturity, they’re built to deliver a return that’s

more explicitly linked to inflation.

The core idea: TIPS help reduce the “inflation surprise” risk in a portfolioespecially for investors who worry about purchasing power more than bragging rights.

So What Happens to “Market Returns” When Inflation Changes?

Here’s the common-sense framing: inflation affects market returns by changing the context in which those returns occur.

It’s not just “prices higher.” It’s:

- Real vs. nominal: inflation can make nominal returns look bigger than the wealth you actually gained.

- Policy response: higher inflation can trigger higher rates, which can pressure valuations and bond prices.

- Profit dynamics: some companies pass through costs; others get squeezed.

- Asset rotation: leadership can shift (growth vs. value, domestic vs. international, long duration vs. short).

- Correlation changes: stocks and bonds can become more correlated when inflation is persistently high, reducing diversification benefits.

That last one is sneaky. Many investors learned the hard way that when inflation is the main macro story, both stocks and bonds can struggle at the same time.

The “classic” diversification relationship can wobble.

A Real-World Snapshot: When Inflation Spiked, Markets Repriced Fast

One of the clearest recent examples came during the early-2020s inflation surge. U.S. consumer prices rose sharply, including a headline CPI reading of

9.1% year-over-year in June 2022a level that grabbed attention far beyond finance Twitter.

Markets didn’t just “dislike inflation” like it was a bad movie sequel. They repriced the entire interest-rate path. Higher expected rates pushed up discount

rates, and both stock and bond markets felt the pressure. U.S. equities had a rough 2022, and many investors were surprised that bonds didn’t cushion the fall

the way they expected.

The lesson isn’t “inflation means doom.” The lesson is: when inflation shifts quickly, markets can adjust quicklyand the adjustment can show up as

volatility and drawdowns, even if long-term outcomes remain reasonable for diversified investors.

Common-Sense Moves to Deal with Inflation (Without Panicking)

1) Measure the right return

Get in the habit of asking: “What did I earn after inflation?” That one question reduces a lot of bad decision-making.

2) Respect diversification, but understand its mood swings

A diversified portfolio still matters. But diversification is not a guarantee that one part of your portfolio will always save the other. In inflation-driven

regimes, correlation patterns can change. The goal becomes resilience, not perfection.

3) Favor quality and pricing power

In inflationary environments, companies that can raise prices without destroying demand tend to hold up better. That often includes businesses with strong brands,

essential services, and sticky customer relationships.

4) Don’t overreact to one data print

Inflation data is noisy. Markets can over-interpret it. Your job (as the human in the loop) is to avoid turning one month’s number into a 10-year identity crisis.

5) If you’re using bonds for safety, think about what kind of safety you need

Bonds can help reduce volatility and fund near-term spending. But if your real concern is purchasing power, consider inflation-aware tools like TIPS as part of

the mix, not as a magic shield.

Friendly note: this is general education, not personal financial advice. If you’re investing as a teen or new investor, it’s smart to discuss plans with a

parent/guardian and consider professional guidance.

Bottom Line: Inflation Changes the Game, Not the Goal

Inflation affects market returns in two big ways: it changes the math (real vs. nominal returns) and it changes the environment

(rates, valuations, profits, and investor psychology).

The common-sense takeawayvery much in the spirit of A Wealth of Common Senseis that you don’t need a perfect inflation forecast to invest well. You need a

process: focus on real returns, avoid overconfidence, diversify intelligently, and resist the urge to “solve” inflation with one dramatic portfolio move.

Inflation is a variable. Your behavior is the strategy.

Experiences: What Inflation Feels Like in Real Portfolios (And What People Learn)

Inflation isn’t experienced as a chart. It’s experienced as a series of tiny moments that add uplike realizing your “usual” grocery run now costs an extra

$30, or noticing your streaming services quietly raised prices again (because apparently the “premium” tier now includes the privilege of paying more).

Investors tend to learn inflation lessons in the same way: not through a single dramatic event, but through repeated surprises that change expectations.

One common experience is the “cash comfort trap.” When headlines get loud, people often build up cash because it feels safe. The problem is that

inflation makes cash a guaranteed loser in real terms. Many investors only notice this after a year or two, when their account balance looks stable but their

lifestyle budget feels tighter. They didn’t “lose money” in nominal termsyet they lost purchasing power. That gap is what drives the feeling of falling behind.

Another big lesson shows up in the “60/40 surprise.” A lot of diversified investors assume bonds always hedge stock risk. In many historical

periods, they did. But when inflation becomes the dominant macro force, rates can rise quicklyand rising rates can push bond prices down at the same time stocks

are repricing lower. Investors who expected bonds to be a shock absorber sometimes experienced them as a second shock. The practical takeaway most people adopt

afterward is more nuanced: bonds are still useful, but you need to know whether you’re using them for near-term spending stability, portfolio ballast,

or inflation protectionbecause those are not always the same thing.

Then there’s the “pricing power revelation.” During inflationary stretches, investors often begin paying closer attention to which companies can

raise prices without losing customers. You’ll hear people describe the moment they “got it”: a business they used every week raised prices, nobody stopped buying,

and earnings held up. That’s when inflation stops being abstract and becomes a filter for understanding business quality. It’s also why some investors shift focus

toward companies with strong brands, essential services, or entrenched network effectsbecause demand that doesn’t disappear at the first price hike is a form of

durability.

Many people also experience inflation through housing and debt. Homeowners with fixed-rate mortgages often report a strange emotional mix: higher

prices feel bad, but their fixed payment feels “lighter” over time as wages and prices rise. Meanwhile, people needing new loans can feel the opposite: higher

interest rates make borrowing much more expensive. That split experience shapes investing behaviorsome lean into real assets, others become more conservative,

and many simply reassess risk because the cost of capital is no longer close to zero.

Finally, there’s the learning curve with inflation-linked instruments. Investors who tried TIPS often discovered they don’t behave like a simple

savings account: prices can move because real yields change, even if the long-term goal is inflation-adjusted protection. The “experience” many describe is

upgrading their expectations from “this should never go down” to “this is a tool with a specific job.” Once framed correctly, TIPS become less about daily price

movement and more about aligning part of a portfolio with future purchasing-power needs.

If there’s a universal lesson across these experiences, it’s this: inflation tests patience and clarity. It pushes investors to separate what feels safe from

what actually protects wealth. And it rewards the boring disciplinesdiversification, rebalancing, focusing on real returnsbecause those habits are designed

for exactly the moments when the world gets financially weird.