Table of Contents >> Show >> Hide

- What “hedging” means in real estate

- Why housing prices fall in the first place

- 1) Build a “do not panic” cash reserve

- 2) Protect your monthly payment before you chase “equity hacks”

- 3) Avoid overusing home equity

- 4) Invest in repairs and upgrades that preserve value, not ego

- 5) Hedge your house by diversifying your wealth away from your house

- 6) Create income from the property when possible

- 7) If you may need to sell, hedge early with strategy, not hope

- 8) Pay attention to insurance and climate risk

- 9) Know your distress options before you need them

- 10) Advanced hedge for investors: reduce one-way real-estate exposure

- Mistakes that make falling home prices hurt more

- The bottom line

- Experience-Based Lessons: What homeowners learn when prices soften

Note: This article is for general informational purposes only and is not legal, tax, investment, or mortgage advice.

If the phrase falling housing prices makes you want to clutch your property-tax bill and whisper, “Not today,” you are not alone. Homeowners do not need a dramatic crash to feel stressed. A soft market can be enough. Listings sit longer. Buyers get pickier. Appraisals come in with less swagger. And suddenly your home, which looked like a financial superhero two years ago, starts acting like a moody stock with shingles.

The good news is that you can hedge falling housing prices. Not in the Hollywood-trader sense where you short your neighbor’s split-level ranch. For most households, a smart housing hedge is much more practical: protect your cash flow, preserve your options, reduce forced-sale risk, and keep your overall wealth from living and dying by one address.

That is the real game. If housing prices dip, the people who suffer most are usually not the ones whose Zestimate got less flattering. It is the people who have to sell at the wrong time, borrowed too aggressively, ignored insurance and maintenance, or treated home equity like an ATM with granite countertops.

This guide breaks down the best ways to hedge against a weaker housing market, with practical strategies for homeowners, would-be sellers, move-up buyers, and small real-estate investors.

What “hedging” means in real estate

In investing, a hedge is an offsetting move that reduces downside risk. In housing, the idea is similar, but the tools are different. Your primary residence is not a liquid security. You cannot click a button and buy a neat little put option on your ZIP code. Housing is local, illiquid, expensive to transact, and emotionally loaded. It is finance wearing a bathrobe.

So a useful housing hedge usually does one or more of these things:

- Reduces the odds that you will be forced to sell during a downturn.

- Protects monthly affordability if rates, taxes, or insurance costs rise.

- Preserves or improves your home’s relative value compared with nearby properties.

- Offsets housing exposure by building wealth outside your home.

- Creates flexibility, such as rental income, refinancing options, or a longer time horizon.

If you remember only one idea from this article, make it this: the best hedge against falling home prices is time plus flexibility. A price dip hurts less when you can comfortably hold the property and wait.

Why housing prices fall in the first place

Housing prices do not fall for one reason. They soften when affordability worsens, when mortgage rates stay elevated, when local job growth weakens, when too much new supply hits one area, or when insurance and climate risk make certain properties less appealing. Sometimes prices do not plunge nationally, but specific metros or neighborhoods cool a lot faster than the headlines suggest.

That distinction matters. Many homeowners prepare for a national crash and ignore the more common risk: a local reset. Maybe your city added thousands of new condos. Maybe buyers in your area suddenly care a lot more about flood risk, HOA dues, school rezoning, or commute patterns. Maybe your house is fine, but five over-ambitious sellers on your street discovered that the market no longer applauds “priced to manifest.”

In other words, housing risk is not just about market direction. It is about timing, leverage, geography, and whether your finances can absorb bad luck without turning it into a crisis.

1) Build a “do not panic” cash reserve

The first and best hedge is boring. That is why it works.

A homeowner with a strong emergency fund can ride out job loss, repairs, temporary vacancies, higher insurance premiums, and surprise expenses without dumping the property into a soft market. A homeowner without cash often has to sell when selling is least attractive. That is not a market problem anymore. That is a timing problem wearing a fake mustache.

A solid target is enough liquid savings to cover several months of total housing costs, not just principal and interest. Include taxes, insurance, utilities, HOA dues, and routine maintenance. If you own rental property, include vacancy and repair reserves too.

This strategy does not make home prices rise, but it dramatically lowers the chance that a price decline becomes a realized loss.

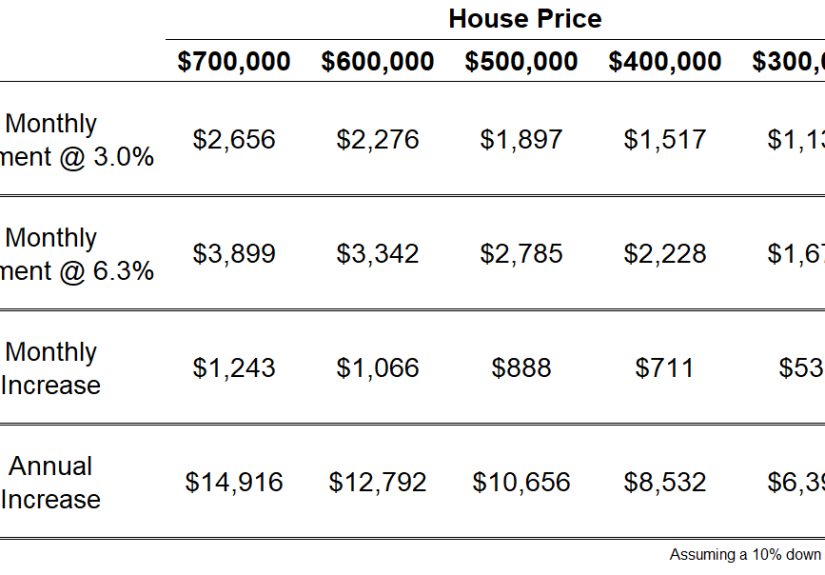

2) Protect your monthly payment before you chase “equity hacks”

When prices feel shaky, payment stability matters more than cleverness. If you have an adjustable-rate mortgage and plan to stay in the home, explore whether refinancing into a fixed-rate loan makes sense. If you already have a low fixed rate, congratulations: you own one of the most valuable anti-chaos devices in modern personal finance.

Other payment-protection moves can include:

- Mortgage recasting after a lump-sum payment, which can lower your monthly bill without replacing your existing low rate.

- Removing expensive consumer debt so your total household obligations are easier to manage.

- Avoiding payment shocks from risky borrowing structures that look affordable only on their best behavior.

Be especially careful with HELOCs, cash-out refinances, and second mortgages. These tools can be useful, but they are not magic. If you borrow against equity and prices later fall, you may have less flexibility to refinance, sell, or weather a rough patch. Debt is fine when it buys resilience. It is dangerous when it buys a kitchen island with a more confident personality than your balance sheet.

3) Avoid overusing home equity

Many owners treat rising home values as spendable wealth. That is understandable, but it is also how people accidentally turn a mild market slowdown into a personal recession.

If you want to hedge falling home prices, one of the smartest things you can do is leave some equity alone. Think of equity as a shock absorber. The more of it you preserve, the more room you have if prices soften, appraisal values slip, or selling costs eat a larger share of the proceeds.

Using equity for a high-value repair, major safety issue, or improvement that keeps the home marketable may be sensible. Using equity to fund lifestyle spending, speculative investments, or debt cycling is much harder to defend.

A good rule of thumb: before borrowing against your house, ask whether the decision would still look smart if your property value dropped 10% and your income got less predictable. If the answer is no, step away from the “unlock your home’s value” ad copy.

4) Invest in repairs and upgrades that preserve value, not ego

In a softer market, buyers become choosy. Homes with deferred maintenance, insurance problems, ugly inspection surprises, or obvious climate vulnerabilities often take the first punch. That means one practical hedge is to make your home easier to insure, finance, and sell.

Focus on improvements that preserve value and reduce future buyer objections:

- Roof, drainage, gutters, and water management

- HVAC, plumbing, electrical, and safety issues

- Energy efficiency that lowers operating costs

- Window, door, and exterior envelope improvements

- Permitted additions or accessory space with legitimate utility

- Wildfire, wind, or flood mitigation where relevant

Notice what is missing from that list: ultra-personal luxury upgrades with questionable resale value. The goal is not to win a design award from your cousin’s Instagram followers. The goal is to preserve marketability and reduce discount pressure if buyers compare your home against newer or better-prepared listings.

5) Hedge your house by diversifying your wealth away from your house

This is the part many homeowners avoid because it sounds unfair. You worked hard to buy a home, so naturally you want it to be the star of the portfolio. But concentration risk is real. If too much of your net worth sits in one property, one city, and one local housing cycle, you are exposed.

A strong hedge is to keep building assets outside real estate: retirement accounts, index funds, cash reserves, short-term bonds, or even a business. That way, if your home’s value stalls or dips, your entire balance sheet is not frozen in sympathy.

This is especially important for people who already work in real estate, construction, lending, or housing-adjacent fields. If your job, your bonus, and your biggest asset all depend on the same housing market, that is not diversification. That is a family reunion of correlated risk.

6) Create income from the property when possible

One of the best ways to hedge a price decline is to improve the cash-producing ability of the property. A house that can offset its own carrying costs is less fragile than one that relies entirely on appreciation.

Depending on local rules and your lifestyle, that might mean:

- Renting a room or finished basement

- Adding an ADU or legal guest unit

- Using house hacking during a temporary budget squeeze

- Choosing a duplex or multi-unit property instead of a purely consumption-oriented home

This approach is not for everyone, and it comes with zoning, tax, landlord, and insurance issues. But from a risk perspective, income is powerful. Appreciation is opinion until you sell. Rent is math.

7) If you may need to sell, hedge early with strategy, not hope

Some homeowners know they may move within a year because of work, family, divorce, retirement, or a new baby who has already claimed the home office and your sleep schedule. If that is you, do not hedge by crossing your fingers. Hedge by preparing for sale before the market forces you to.

Steps that can reduce downside before a sale

- Fix obvious defects before listing.

- Price realistically from day one; stale listings attract discounts.

- Keep enough cash for buyer concessions, moving costs, and overlap months.

- Learn the tax rules on home-sale gain exclusions and timing.

- Compare selling now versus renting the home for a period if local math supports it.

A common mistake is assuming a small price dip is the only cost that matters. In reality, selling expenses, concessions, repairs, vacant months, and carrying costs can do just as much damage. A homeowner who plans ahead may accept a slightly lower price but still keep more money because the process is cleaner and faster.

8) Pay attention to insurance and climate risk

In some markets, the biggest threat to value is not mortgage rates. It is insurability. If a home becomes more expensive to insure, harder to finance, or more vulnerable to flood, fire, or wind damage, buyers may demand discounts even in an otherwise stable market.

That makes risk mitigation a genuine hedge. Review your coverage. Document upgrades. Understand flood-zone issues, roof age, defensible space, drainage, and local building-code expectations. In some cases, resilience improvements can protect both your home’s condition and its future buyer pool.

Think of it this way: a house that is cheaper to own, easier to insure, and less scary to inspect is often worth more relative to competing homes when markets cool.

9) Know your distress options before you need them

The most painful housing losses usually happen when owners wait too long to act. If income drops, payments become difficult, or a refinance no longer works, contact your servicer early. Explore loan modification, forbearance, repayment plans, or FHA loss mitigation if applicable. HUD-approved housing counselors can also help homeowners understand options before foreclosure risk spirals.

This may not sound like a “hedge,” but it absolutely is. The earlier you respond, the more choices you usually keep. Distress becomes expensive when time runs out.

10) Advanced hedge for investors: reduce one-way real-estate exposure

For real-estate investors, a more traditional hedge may make sense. That could include diversifying across regions, property types, lease structures, and tenant profiles. Some investors also balance direct property holdings with more liquid assets so they are not forced sellers when cap rates move or lending conditions tighten.

Could a sophisticated investor hedge housing exposure with public securities, mortgage-related assets, or bearish real-estate positions? In theory, yes. In practice, the match is rarely perfect for ordinary households. Your specific property risk in Phoenix, Tampa, or suburban Chicago is not going to move in lockstep with a national trade. For most owners, strong personal finance still beats clever market theater.

Mistakes that make falling home prices hurt more

- Assuming national averages describe your neighborhood.

- Borrowing aggressively during a period of rising values.

- Ignoring taxes, insurance, and maintenance when calculating affordability.

- Over-improving the property for personal taste instead of marketability.

- Waiting until financial stress becomes urgent before calling the lender.

- Keeping nearly all wealth tied to one home.

The bottom line

If you want to hedge falling housing prices, stop looking for a single silver bullet. There usually is not one. The winning approach is layered. Protect the payment. Keep real cash reserves. Preserve equity. Improve insurability and condition. Diversify your wealth. Add income potential where practical. And if a sale may be coming, prepare early instead of negotiating with reality at the eleventh hour.

A home is both shelter and finance. That combination is why housing feels personal when prices wobble. But a calmer, systems-based approach works better than fear. The goal is not to predict every housing headline. The goal is to make sure your household can handle a softer market without making desperate decisions.

That is the true hedge: not perfection, but resilience.

Experience-Based Lessons: What homeowners learn when prices soften

One of the most useful lessons from homeowners who have lived through a cooling market is that psychology matters almost as much as math. When prices are rising, people assume they are strategic geniuses. When prices flatten, they suddenly become amateur economists with insomnia. In reality, the households that fare best are usually the ones that made calm decisions before the headlines turned dramatic.

Consider the owner who bought a modest house with a fixed-rate mortgage, kept a real emergency fund, and never treated appreciation as spendable income. When nearby homes dropped in value, that owner was annoyed, of course, but not trapped. The monthly payment still worked. Repairs still got done. Selling could wait. In a softer market, patience often acts like invisible equity.

Now compare that with the homeowner who pulled cash out twice during boom years, financed cosmetic projects at peak contractor pricing, and assumed a future sale would clean up every questionable choice. When the market cooled, the problem was not only the lower price. It was the lack of room. Less equity meant fewer refinancing options, less negotiation power, and more anxiety around every unexpected expense.

Small landlords learn similar lessons. The experienced ones do not underwrite a rental based on heroic appreciation. They assume turnover, repairs, insurance surprises, and the occasional water heater with terrible timing. Because of that, they can hold through weak periods. The inexperienced ones often discover that a “cash-flowing” property was really a spreadsheet costume held together by optimistic rent assumptions and emotional support from the word “passive.”

Another common experience involves sellers who wait too long to adjust. In a slowing market, the first price cut is strategy; the fourth price cut is biography. Homeowners who prepare early, repair obvious issues, study comparable sales honestly, and price near reality often preserve more equity than sellers who start high and chase the market down month by month.

There is also a quieter lesson from families who stay put. They often find that a home becomes less risky over time when life around it becomes stronger. Income rises. Principal gets paid down. Savings grow. The neighborhood improves. The child who once needed a nursery suddenly needs college money and steals all the snacks. Over the years, the same house that felt financially fragile can become stable simply because the owners gave themselves enough runway.

That is why experienced homeowners tend to sound less dramatic than first-time market watchers. They know that a temporary dip is uncomfortable, but a forced move is what really does damage. They know a clean roof matters more than hot market gossip. They know insurance paperwork can matter more than a designer faucet. And they know that the best hedge is often not a flashy move, but a series of sensible decisions that keep options open when everyone else is busy panicking on the internet.