Table of Contents >> Show >> Hide

- What a Sell-Off Really Is (And Why It Feels Like a Personal Attack)

- Why Sell-Offs Hit Hard: The Brain’s Greatest “Feature” (Loss Aversion)

- Ben Carlson’s “Price Explains the Mood” Idea

- The Cast of Characters in Your Head During a Sell-Off

- Corrections Are Common; Crashes Are Not (But Your Emotions Treat Them the Same)

- A Common-Sense Framework for Handling a Market Sell-Off

- Specific Sell-Off Scenarios (And What Common Sense Looks Like)

- How to Tell If You’re Panicking (A Quick Checklist)

- The Most Underrated Skill in a Sell-Off: Behavioral Coaching (Even If You Coach Yourself)

- Real-World Experiences During a Sell-Off (What It Feels Like, and What Actually Helps)

- Conclusion: Your Portfolio Needs a Plan, Not a Mood

A sell-off has a special talent: it turns otherwise reasonable humans into caffeine-fueled fortune-tellers who suddenly “just know” what the market will do next.

One day you’re calmly investing for the long term; the next, you’re doomscrolling headlines at 1:17 a.m., convinced your portfolio is personally beefing with you.

If that sounds familiar, welcome to the clubmembership is free, and the snacks are mostly stress.

The good news is that the feelings you have during a market sell-offfear, regret, panic, “why did I ever buy that?”are common and well-studied.

The better news is you can build a simple, repeatable way to respond without turning “volatility” into “self-sabotage.”

This guide breaks down what’s happening in your brain, why sell-offs feel so loud, and what “common sense” looks like when prices are doing backflips.

What a Sell-Off Really Is (And Why It Feels Like a Personal Attack)

A sell-off is a period when many investors rush to sell, pushing prices down quickly. Sometimes it’s a garden-variety correction (painful but normal).

Sometimes it grows into a bear market (longer, uglier). And sometimes it becomes a true crisis (rare, but it happens).

The psychological kicker is that markets are a scoreboard that updates every second. Most parts of life don’t do that.

Your job doesn’t send you a push notification every 30 seconds: “Your career is down 2.3% since lunch.”

But your brokerage app absolutely willand it will do it with the enthusiasm of a toddler with a drum set.

Why Sell-Offs Hit Hard: The Brain’s Greatest “Feature” (Loss Aversion)

Behavioral finance has a core idea that explains a lot of bad investing decisions: losses feel worse than equivalent gains feel good.

In plain English, losing $1,000 hurts more than gaining $1,000 feels awesome. That’s loss aversion.

It’s one reason investors are tempted to “make the pain stop” by sellingespecially when the market is dropping fast.

Loss aversion turns a temporary decline into a threat signal. Your brain isn’t trying to optimize your retirement plan; it’s trying to protect you from discomfort.

That’s helpful when you’re avoiding an actual bear in the woods. It’s less helpful when you’re avoiding a red number on a screen.

Sell-Off Mind Trick #1: “If I Sell Now, I Can Control It”

During a downturn, selling feels like taking actionand action feels like control.

But in investing, “doing something” is not automatically “doing something smart.”

Panic selling can lock in losses and make it harder to participate in the eventual rebound (which often arrives while everyone is still arguing online).

Sell-Off Mind Trick #2: Recency Bias (The Market Will Do Tomorrow What It Did Today)

Recency bias is the habit of over-weighting what just happened. If the market fell for five days, your brain starts writing a screenplay called

The Market Falls Forever: Part II. The story feels true because it’s fresh, vivid, and emotionally charged.

Unfortunately, markets don’t care about your story arc.

Ben Carlson’s “Price Explains the Mood” Idea

One of the most useful ways to think about sell-offs is this: price changes investor behavior.

After huge gains, it’s easier to find a reason to sell and “lock it in.” After big losses, it’s easier to find a reason to buyeven if the news is still bleak.

Market psychology swings like a pendulum, and price is often the hand pushing it.

Consider the emotional whiplash of a big run followed by a drop. If you’ve watched an index soar for years, you start to believe that’s normal.

Expectations inflate. Risk feels invisible. Then a sell-off arrives and reminds everyone that markets are not a straight linemore like a long hike with occasional surprise staircases.

Example: When “Phenomenal Returns” Set the Stage for Panic

Carlson points out that the S&P 500 posted very strong returns across 2019–2021, and the Nasdaq 100 was also exceptionally strong in that stretch.

When returns are that good for that long, expectations can drift away from realityso a sell-off feels shocking, even if it’s statistically normal.

Example: 1987’s Crash Wasn’t Just “One Bad Day”

Black Monday is often remembered as a single terrifying day, but the setup matters.

When markets have had a huge run and valuations and expectations are elevated, investors can become jumpy.

Add a catalyst (rates, structural market issues, scary headlines) and fear spreads faster than a group text.

The Cast of Characters in Your Head During a Sell-Off

1) Herding: “Everyone Is Selling… So Should I?”

Herding bias is the urge to follow the crowd. It’s powerful because being wrong alone feels worse than being wrong together.

In a sell-off, you’ll hear it as: “Maybe the market knows something I don’t.”

Sometimes the market does know something. Sometimes the market is just having feelingsloud ones.

2) Availability Bias: “The Scariest Headline Must Be the Most Likely Outcome”

When scary information is easy to recall, it feels more probable. In sell-offs, headlines get intense because attention is the currency.

Your brain then confuses “popular news” with “probable future.”

3) Regret Aversion: “If I Don’t Sell and It Drops Again, I’ll Hate Myself”

Regret aversion makes you take action to avoid future self-blame. It can push you into panic selling (“I’ll feel dumb if this gets worse”)

or into paralysis (“I’m scared to do anything”).

Either way, regret becomes the driver, not your plan.

4) The Disposition Effect: “Sell Winners Too Soon, Hold Losers Too Long”

Many investors feel an urge to “take profits” quickly (so they can feel smart) and to avoid realizing losses (so they can avoid feeling wrong).

Over time, this can lead to odd behavior: trimming what’s working and clinging to what isn’t.

In sell-offs, the disposition effect can get louder because everything looks like a losereven investments that still make sense long-term.

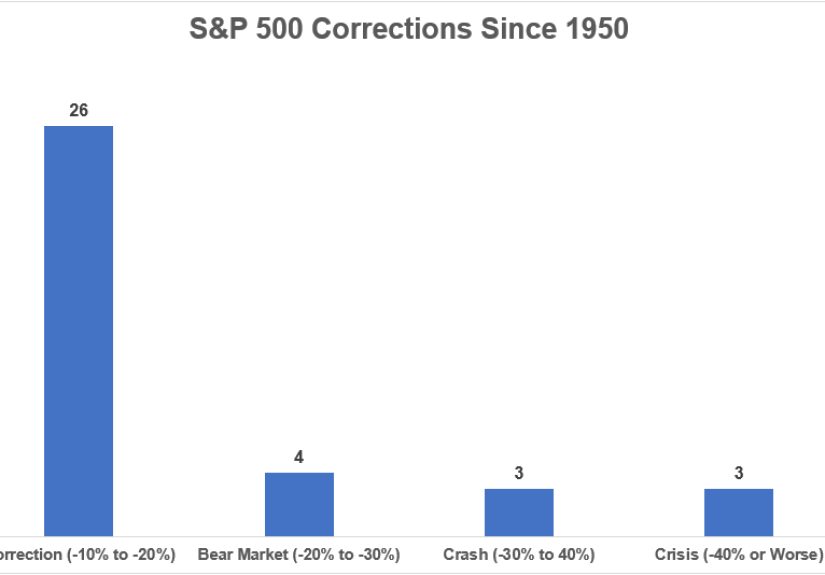

Corrections Are Common; Crashes Are Not (But Your Emotions Treat Them the Same)

A practical “wealth of common sense” reminder: markets fall a lot. Not always catastrophically, but regularly enough that it shouldn’t be shocking.

The hard part is that your nervous system doesn’t care whether this is correction #37 or the apocalypseit reacts to the red numbers.

That’s why a sell-off plan should be built before you need it, when you’re not emotionally negotiating with your portfolio.

The goal is not to “feel nothing.” The goal is to feel the feelings and follow the plan anyway.

A Common-Sense Framework for Handling a Market Sell-Off

Step 1: Name the Game You’re Playing

Are you investing for 20–30 years (retirement)? Or are you trading for weeks (speculation)?

Sell-offs punish confusion. A long-term investor acting like a day trader is like bringing a spoon to a sword fight: technically an option, not a good one.

Step 2: Translate Fear Into Numbers

Fear is vague. Numbers are specific. Instead of “I’m down a lot,” look at:

- Your current allocation (stocks/bonds/cash)

- Your time horizon (years until you need the money)

- Your required return (what you actually need to meet your goals)

- Your plan for rebalancing (if stocks drop, do you buy a bit to restore targets?)

This shifts you from “reacting to the market” to “running a process.”

Step 3: Reduce the Number of Bad Decisions Available

In a sell-off, your biggest enemy is often you with too many buttons.

Consider guardrails:

- Limit portfolio checking to once per week (or once per month if you want extra peace).

- Remove trading apps from your home screen (out of sight, fewer midnight “ideas”).

- Use automatic investing (dollar-cost averaging) so discipline happens without motivation.

Step 4: Remember the “Best Days” Problem

Many studies and investor education pieces highlight the same pattern: some of the market’s strongest up days cluster near its worst down days.

If you panic sell after the drop, you increase the odds you’ll miss the reboundbecause rebounds are rude like that. They arrive unannounced.

Step 5: Rebalance Like a Robot (Politely)

Rebalancing is the unglamorous hero of sell-offs. It forces you to do the opposite of panic:

trim what held up better and add to what fellwithin your risk limits.

It’s not exciting. That’s why it works. Excitement is usually expensive.

Step 6: Keep Cash for Life, Not for Drama

One reason sell-offs cause panic is practical: people worry they’ll need money soon.

A healthy emergency fund (and short-term cash needs separated from long-term investments) can prevent “selling stocks to pay rent,”

which is the worst kind of forced timing.

Specific Sell-Off Scenarios (And What Common Sense Looks Like)

Scenario A: “Everything Is Down. I Want to Move to Cash.”

Common-sense response: If your time horizon is long, moving to cash after prices fell may lock in the decline.

Ask: “What would need to be true for me to buy back in?” If you don’t have a clear, rules-based answer,

you may be making an emotional trade dressed up as a strategy.

Scenario B: “I Knew This Would Happen. I Should Have Sold Earlier.”

Common-sense response: Hindsight is a loud liar. The market offers infinite “I should have” moments.

Instead of rewriting the past, upgrade the process:

diversify, rebalance, automate contributions, and align risk with what you can actually tolerate.

Scenario C: “I Want to Buy the Dip, But I’m Scared.”

Common-sense response: If you’re adding risk, do it in a way that matches your plan.

For many investors, that means steady contributions (dollar-cost averaging) rather than one giant “all-in” moment.

You don’t need perfect timing; you need consistent behavior.

How to Tell If You’re Panicking (A Quick Checklist)

- You’re making decisions faster than you can explain them.

- You’re using phrases like “this time is different” without data.

- You’re checking prices more often than you check your sleep.

- You’re building a plan around headlines instead of goals.

- You feel relief at the thought of selling (temporary calm can be an expensive emotion).

The Most Underrated Skill in a Sell-Off: Behavioral Coaching (Even If You Coach Yourself)

The investing world increasingly acknowledges a simple truth: your portfolio’s biggest risk factor is not always the marketit’s behavior.

That’s why many firms emphasize “staying the course,” maintaining focus on long-term goals, and using structured coaching during volatility.

You can DIY a version of that coaching with two tools:

(1) a written plan you trust, and (2) a short script you read when the market is melting down.

For example:

“My portfolio is built for decades, not days. Volatility is the fee I pay for long-term growth. I will follow my rebalancing rules and keep investing.”

Yes, it’s cheesy. So is flossing. Still works.

Real-World Experiences During a Sell-Off (What It Feels Like, and What Actually Helps)

Below are experiences many investors describe during sell-offs. These are not “perfect investor” stories.

They’re the messy, human onesthe kind where your brain argues with your spreadsheet and your emotions try to start a coup.

Experience #1: The “I Can’t Look” Phase.

In the early days of a sharp drop, a lot of people stop checking accounts entirely. That can be healthyuntil it turns into avoidance.

The helpful version looks like this: “I’m limiting checks to once a week, and I’m sticking to my automated contributions.”

The unhelpful version looks like: “I refuse to open my statements for six months, and I’ll decide later.”

The difference is whether you still have a process running in the background.

Experience #2: The Headline Whiplash.

Sell-offs often come with a rotating cast of scary narratives: inflation, rates, recessions, geopolitics, banking stress, tech bubbles, you name it.

Many investors notice that the story changes daily, but the emotional effect stays the same: urgency.

What helps is separating “news risk” from “plan risk.”

News risk is the market being dramatic. Plan risk is you having too much stock exposure for your real comfort level.

If the sell-off reveals you can’t sleep, that’s useful informationnot a reason to blow up your strategy, but a reason to right-size it.

Experience #3: The “Get Me to Cash” Bargain.

A common thought pattern is: “If I just sell now, I can buy back lower.”

People who try it often discover the hard part isn’t sellingit’s buying again.

When prices keep dropping, you feel “smart” and want to wait for an even better deal.

When prices bounce, you feel “tricked” and want to wait for confirmation.

The market can climb a long way while investors wait for feelings to become certain.

That’s why many long-term investors prefer rules over predictions: scheduled contributions, rebalancing bands, and clear time horizons.

Experience #4: The Surprise Rally (a.k.a. “Where Did That Come From?”).

Investors often report that the strongest up days feel emotionally suspicious.

After a week of losses, a big green day can feel like a trapbecause your brain expects more pain.

But sharp rallies are a normal feature of volatile markets. People who bailed out frequently describe the same frustration:

they waited for “stability,” and by the time it arrived, prices were higher.

The practical takeaway isn’t “always buy.” It’s “don’t build your plan on emotional timing.”

Experience #5: The Quiet Confidence of a Boring Plan.

The investors who tend to cope best aren’t fearless; they’re prepared.

They usually have (1) a diversified allocation they understand, (2) an emergency fund so they’re not forced to sell, and (3) a simple policy:

keep investing, rebalance occasionally, ignore the noise.

In sell-offs, boring becomes a superpower. The market is putting on a fireworks show; your job is to not run into the street.

If there’s one universal “experience lesson,” it’s this: sell-offs don’t just test your portfoliothey test your identity.

You want to see yourself as rational, disciplined, long-term. A sell-off tries to rename you “impulsive headline mammal.”

The win is not having zero fear. The win is building routines that keep fear from driving.

Conclusion: Your Portfolio Needs a Plan, Not a Mood

Investor psychology during a sell-off is not a character flawit’s human wiring meeting a high-speed price machine.

The market drops, your brain screams, and your finger hovers over the sell button like it’s defusing a bomb.

The way through is common sense: align risk with your life, automate good behavior, rebalance with rules, and keep your eyes on the horizon.

Sell-offs will happen again. The question is whether you’ll treat them like a surprise attack or like a normal (if unpleasant) feature of long-term investing.

You can’t control the market. But you can control your processand that’s usually where the real returns are hiding.