Table of Contents >> Show >> Hide

- Why “Six Figures” Still Feels Like a Big Deal

- First, Define “Rich”: Income, Net Worth, or Freedom?

- What the Data Suggests: Where Six Figures Sits in the U.S.

- The Zip Code Tax: Cost of Living Turns $100K Into Different People

- Taxes: The Part of Six Figures Nobody Brags About

- Life Stage Matters: Single, Partnered, Kids, and the Childcare Plot Twist

- The HENRY Trap: High Earners, Not Rich Yet

- How to Turn Six Figures Into Wealth (Instead of a Very Nice Monthly Burn)

- So… Is Making $100,000 a Year Rich?

- Bonus Add-On: Real-World Six-Figure Experiences (About )

- Conclusion

- SEO Tags

“Six figures” used to be the financial equivalent of walking into a party wearing sunglasses at night: a little dramatic,

slightly mysterious, and universally assumed to mean you’re doing great. Then life happened. Rent went up, childcare started

costlier-than-a-used-car, and groceries began charging “because we can” fees.

So… is making six figures a year considered rich? The most honest answer is: sometimes. The most useful answer is:

it depends on your zip code, your lifestyle, and whether your money is building wealth or just funding an expensive treadmill.

Let’s break it downFinancial Samurai style: practical, slightly skeptical, and allergic to financial delusion.

Why “Six Figures” Still Feels Like a Big Deal

Humans love clean milestones. Six figures has that crisp, cinematic vibe: $100,000+. It sounds like you’ve “made it,” even if your

bank account disagrees every time your mortgage, student loans, or toddler’s daycare invoice shows up like a jump scare.

The catch: “six figures” is a range so wide it’s basically a freeway. $100,000 and $900,000 both qualify, but they live in totally

different universes. One is “I can finally breathe.” The other is “I can finally buy the air.”

A better question is: What does your six-figure income actually buy after taxes and real-world costs? Because rich isn’t a salary.

Rich is what’s left overtime, flexibility, and options.

First, Define “Rich”: Income, Net Worth, or Freedom?

Income is a snapshot (and it lies sometimes)

Income tells you what you earned this year, not what you kept, not what you own, and definitely not how much control you have over your life.

Plenty of people earn $120K and feel broke. Plenty earn $80K and feel calm. The difference is often fixed costs, debt, and habits.

Net worth is the movie (and it’s harder to fake)

Net worthassets minus liabilitiesis the scorecard that reflects how long you’ve been turning income into something that can support you

without constant hustle. Two people can earn the same six-figure salary; the one saving and investing consistently becomes wealthy. The one

upgrading everything on autopilot becomes a very polite hostage to their monthly bills.

Financial independence is the endgame

If you can cover your living expenses without needing your paycheck, you’re rich in the way that matters. It’s not a champagne-spraying yacht

definition. It’s the “I can quit a toxic job without panic” definition. It’s the “I can take a sabbatical” definition. It’s the

“my calendar belongs to me” definition.

What the Data Suggests: Where Six Figures Sits in the U.S.

Let’s anchor this in reality. Recent U.S. income data puts median household income in the low-to-mid $80Ks. That means $100K is

above the midpointbut not by an “I’m rich!” margin. In many places, it’s closer to “solidly comfortable” than “private jet.”

Six figures vs. “upper income”

One helpful lens: income tiers. Research that adjusts for household size often places “upper income” (sometimes casually called “upper class” in

popular conversation) at more than roughly double the median. Using that kind of framework, $100K may still fall inside

“middle-income” for many householdsespecially familieswhile higher six figures can push you into upper-income territory.

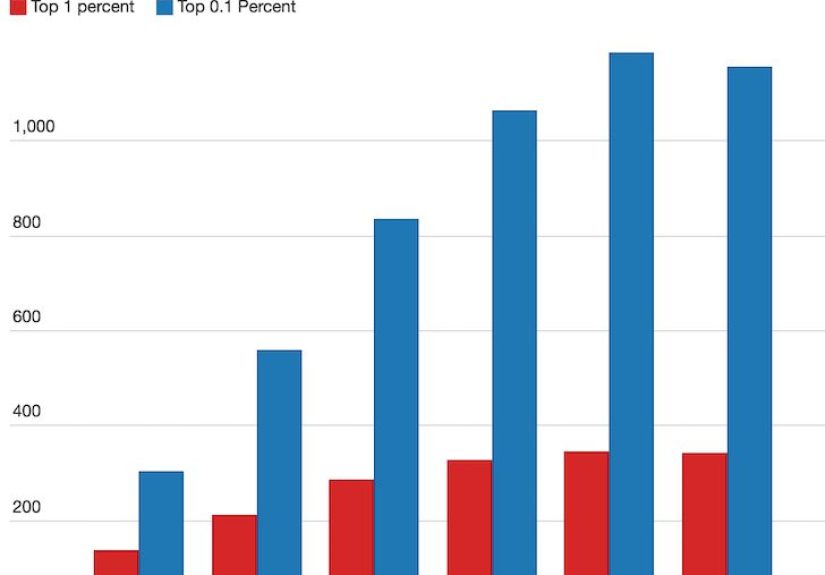

Top earner benchmarks (a reality check)

If you’re looking for “nationally rich,” you’re usually talking top deciles. Benchmarks for the top 10% by income are far above $100K.

That’s why so many six-figure earners describe themselves as “fine” or even “stretched,” depending on costs.

The takeaway: $100K is meaningful, but it’s not automatically wealthy. In the U.S. today, it’s better described as a

strong income foundationone that can build wealth if your spending doesn’t expand to match it.

The Zip Code Tax: Cost of Living Turns $100K Into Different People

Here’s the quiet truth: the U.S. doesn’t have one cost of living. It has a hundred. Your salary isn’t just a numberit’s a number

multiplied by your location.

$100K in Manhattan vs. $100K in Oklahoma City

Studies comparing purchasing power across cities routinely show that $100,000 can shrink dramatically in the most expensive places after

factoring in taxes and local price levels. In some high-cost urban cores, six figures can feel like “high income, low serenity.”

In lower-cost metros, that same income can create breathing room and actual savings momentum.

Living wage math: “comfortable” depends on household size

Tools that estimate living costs by county and family type show what many people feel: a single adult can often do fine on less than $100K in

many areas, but a household with kids faces a very different cost structure (housing, healthcare, childcare, transportation, and the

unstoppable snack budget).

Translation: six figures can be rich in the right place, and merely adequate in the wrong one. That’s not you “doing it wrong.”

That’s geography doing what it does best: charging rent.

Taxes: The Part of Six Figures Nobody Brags About

When people ask, “Is $100K rich?” they often mean gross pay. Your life runs on net pay. Federal income taxes, payroll taxes,

and (depending on where you live) state and local taxes can turn a $100K salary into a much smaller take-home number. Then benefits come out.

Then you remember you still need to eat.

A practical way to think about it

Instead of obsessing over the gross figure, ask:

After taxes, housing, transportation, and basic needshow much margin do I have?

Margin is the difference between “high earner” and “wealth builder.”

If your margin is small, your strategy might be: reduce fixed costs, avoid lifestyle creep, and use pre-tax retirement accounts and

employer benefits wisely. If your margin is large, your strategy is simpler: don’t sabotage it with a luxury car that eats your future.

Life Stage Matters: Single, Partnered, Kids, and the Childcare Plot Twist

Two people can earn $110K and experience completely different realities:

- Single in a moderate-cost city: six figures can feel like stability, travel, and steady investing.

- Single in a high-cost city: it can feel like you’re doing well… while still renting forever.

- Dual income, no kids: the famous “DINK” advantagemore margin, faster compounding, more options.

- Kids: still wonderful, still expensive, still somehow always hungry.

This is why a “rich” label based purely on salary misses the point. Rich is not just what you earnit’s what your household needs, what you owe,

and what you’re building.

The HENRY Trap: High Earners, Not Rich Yet

There’s a term for people who earn a lot but don’t feel wealthy: HENRYHigh Earners, Not Rich Yet. The label exists because it’s common:

strong income, weak wealth.

How people become HENRYs (without trying)

- Housing inflation + upgrading: buying the maximum house the bank “approves.”

- Lifestyle creep: every raise becomes a subscription to a fancier life.

- Debt stacking: car loans, consumer debt, and “I deserved it” purchases.

- Opportunity cost blindness: ignoring what that spending could become if invested.

The fix is not misery. The fix is intention: spending on what you genuinely value, cutting what you don’t, and paying your future self like it’s a bill.

How to Turn Six Figures Into Wealth (Instead of a Very Nice Monthly Burn)

1) Build a “margin first” budget

Most budgets start with spending and hope savings “works out.” Flip it. Decide what you want to save and invest, automate it, and live on the rest.

If that sounds intense, remember: the alternative is working forever while your couch gets nicer every year.

2) Use retirement accounts like they’re cheat codes (because they kind of are)

Many wealth-building households rely on consistent retirement investing. Some retirement guidelines suggest benchmarks like having multiples of your salary

saved by certain ages. Don’t treat them as a judgmenttreat them as direction. If you’re behind, the answer is rarely “panic.” It’s usually

“increase contributions steadily and reduce high-friction spending.”

3) Avoid the big three wealth leaks

- Overbuying housing (especially in high-cost areas).

- Overspending on cars (the stealth wealth assassin).

- Carrying high-interest debt (a treadmill with extra incline).

4) Treat raises as a wealth accelerator, not a lifestyle coupon

If you’re already living fine, the next raise is a chance to speed-run wealth creation. A simple approach is to split raises:

some for lifestyle (enjoy your life), some for investing (buy your freedom).

5) Measure “rich” with a personal number

Some surveys find Americans associate “wealthy” with a multi-million-dollar net worth, and “comfortable” with a far lower figure. Those are perceptions,

but they’re a helpful reminder: rich is often a net worth and security conversation, not a salary conversation.

So… Is Making $100,000 a Year Rich?

If you’re making exactly $100,000, you’re in a strong position compared with the median householdbut “rich” is still a stretch as a universal label.

In a lower-cost area with manageable housing and no big debt, $100K can feel rich. In a high-cost city with rent, childcare, and student loans,

it can feel like “I make good money… why do I still check my bank app like it’s a horror movie?”

A cleaner answer is:

Six figures can be a great income. Rich is when your wealth (not just your salary) can buy you time.

If you want the Financial Samurai-style goalpost: focus less on the label and more on the outcomehigh savings rate, growing net worth,

diversified investing, and optionality. The real flex is not your income. It’s your freedom.

Bonus Add-On: Real-World Six-Figure Experiences (About )

Below are a few common “six-figure life” experiences people sharecomposites that reflect what many households describe, especially when

comparing different cities, family situations, and money habits.

The “I Finally Hit $100K… Why Doesn’t It Feel Like a Movie?” Story

This one usually starts with pride and ends with a spreadsheet. The paycheck is bigger, sure, but so are the deductions: health insurance,

retirement contributions (hopefully), payroll taxes, and then the real-world stuffrent that rose again, groceries that got weirdly expensive,

and the social pressure to “upgrade” because you’re “in that bracket now.” The best version of this story is when someone notices the drift early

and decides to lock in a higher savings rate before lifestyle creep claims the whole raise. The worst version ends with a luxury car lease and

a permanent case of “Where did my money go?”

The “Two Six-Figure Households Are Not the Same Species” Story

A couple earns $220K combined in a medium-cost city and feels like they’ve hacked life. Another couple earns the same in a high-cost coastal metro

and feels like they’re renting their own existence. The difference is rarely willpower; it’s housing costs, taxes, commute, and childcare.

People often underestimate how much fixed costs shape emotional wellbeing. In lower-cost areas, the margin turns into investing, travel, and

less financial stress. In high-cost areas, the margin gets swallowed by “baseline” livingstill safe, still respectable, but not necessarily rich.

The “Kids Turn Six Figures Into Five Figures” Story

Parents describe six figures as a phase shift: before kids, it feels abundant; after kids, it feels allocated. Childcare can rival a second rent

payment. Activities, healthcare, and the constant need to size-up everything (shoes, clothes, snacks, vehicles, bedrooms) create a steady drain.

Many families find that earning more helps, but not as much as expectedbecause the surrounding ecosystem (housing and services) scales up too.

The families who feel “rich” aren’t always the highest earners; they’re the ones who keep big costs reasonable and automate investing so wealth

still grows during the busy years.

The “Six Figures Finally Worked… When I Stopped Buying Status” Story

This is the glow-up story: someone realizes that looking rich is expensive and being rich is quiet. They downshift the car, negotiate housing,

limit recurring subscriptions, and redirect the savings into retirement accounts and taxable investing. A year later they don’t just have a higher

net worththey have a lower stress level. The psychological win is huge: money stops feeling like something that disappears and starts feeling like

something that accumulates. That’s when six figures stops being a fragile identity and becomes a durable tool.

Conclusion

Making six figures can be a major milestonebut it’s not an automatic “rich” badge. In the U.S., $100K can mean comfort in one zip code and

constant pressure in another. Taxes, housing, family size, and debt can turn “high income” into “high obligations” fast.

If you want a definition that won’t betray you: rich is having margin, assets, and choices. Use six figures to buy those things

not just nicer versions of the same monthly bills.