Table of Contents >> Show >> Hide

- 1) Interest rates: the price of “future money”

- 2) Fiscal stimulus: the government’s “big lever”

- 3) Inflation: the silent editor of every return

- 4) The Fed: not just ratesliquidity, plumbing, and psychology

- 5) Automated investing: the “relentless bid” era grows up

- 6) Demographics: the slow-motion force that doesn’t stop

- 7) Inequality: markets aren’t separate from society

- Putting the seven together: a practical market lens

- Conclusion

- Real-World Experiences: How These Seven Forces Show Up (and Mess With People)

- SEO Tags

Markets love to cosplay as chaos. One day it’s “AI will eat the world,” the next it’s “rates will eat AI,” and by Friday it’s “actually…maybe both?”

But beneath the daily drama, the long-run drivers are surprisingly consistent. In fact, one of the cleanest “zoom-out” frameworks comes from a simple idea:

stop trying to predict every headline and focus on the big levers that repeatedly shape returns, risk, and investor behavior.

[1]

Below are seven forces that keep showing upwhether you’re looking at stocks, bonds, real estate, or the mood swings of your group chat after a red day.

We’ll keep it practical, a little funny, and very focused on what actually moves markets over time (not what trends on social media for 12 minutes).

Quick map of the seven:

- Interest rates

- Fiscal stimulus (and deficits)

- Inflation

- The Federal Reserve (beyond just rates)

- Automated investing (the “relentless bid” era)

- Demographics

- Inequality

1) Interest rates: the price of “future money”

Interest rates aren’t just a bond market thing. They’re the price tag on time itself.

When rates rise, future cash flows get discounted harder, borrowing becomes pricier, and “risk-free” starts competing with “risky but exciting.”

When rates fall, the opposite happensmoney gets cheaper, valuation math loosens up, and investors suddenly rediscover their inner optimist.

[2][3]

Why this matters going forward

The last few years reminded everyone that “rates don’t matter anymore” is one of history’s funnier jokes.

A world where the 10-year Treasury yield sits around the mid-4% range and policy rates aren’t near zero changes portfolio math, corporate finance decisions,

and even the behavior of ordinary savers who can finally earn something on cash.

[2][3]

Specific example

If you’re building a portfolio, starting yield is a big deal for bonds because it’s a major contributor to expected long-term returns.

Higher starting yields can create a “coupon cushion,” meaning modest rate moves don’t dominate outcomes the way they did when yields were pinned to the floor.

[12]

What to watch

- The yield curve (short rates vs. long rates)

- Real yields (rates after adjusting for inflation expectations)

- Credit spreads (how much extra yield investors demand to take corporate risk)

2) Fiscal stimulus: the government’s “big lever”

Fiscal policy used to feel like background noise to marketsimportant, but slow. Then crises hit and fiscal stimulus became the economic equivalent of a firehose.

When the government spends aggressively (or cuts taxes dramatically), it can boost demand, stabilize incomes, and change the depth and duration of downturns.

[1]

Why this matters going forward

Here’s the tension: fiscal support can soften recessions, but persistent deficits and higher interest costs can crowd out other priorities over time.

Markets care because the fiscal path influences growth, inflation pressure, Treasury issuance, and (eventually) political choices about taxes and spending.

[11]

Specific example

When deficits are large and the Treasury needs to issue a lot of debt, it can affect yields and liquidity conditionsespecially if demand from buyers

(households, institutions, overseas investors) doesn’t keep pace smoothly.

[11]

What to watch

- Federal deficit trends and debt servicing costs

- Major spending bills, tax policy shifts, and automatic stabilizers

- Treasury issuance patterns and auction demand

3) Inflation: the silent editor of every return

Inflation is the sneakiest market force because it doesn’t just change pricesit rewrites the meaning of “return.”

A 7% gain sounds great until inflation was 6% and your “real return” basically bought you a fancy cup of coffee and a shrug.

[4]

Why this matters going forward

Inflation influences interest rates, profit margins, wage negotiations, and consumer behavior.

It also shapes what central banks do next, which shapes what markets do next, which shapes what investors do nextyes, it’s a chain reaction.

Recent data has shown inflation cooling compared to the peak, but not necessarily returning to a perfectly calm, “textbook” world overnight.

[4][10]

Specific example

In the latest CPI report (12-month basis), inflation has been in a more moderate range than the surge earlier in the decade, reinforcing that inflation can move in regimes:

“quiet,” “loud,” and “quiet-ish but still annoying.”

[4]

What to watch

- Core inflation vs. headline inflation

- Shelter, services, and wage growth dynamics

- Inflation expectations (what households and markets believe will happen)

4) The Fed: not just ratesliquidity, plumbing, and psychology

The Federal Reserve doesn’t only set a policy rate. It also runs the “plumbing” that keeps short-term funding markets functioning.

And sometimes, it changes its toolkit in ways that affect risk-taking, liquidity, and volatility.

[1][5][6]

Why this matters going forward

The Fed’s balance sheet policy can tighten or ease financial conditions even when the policy rate is unchanged.

Decisions about ending or adjusting balance sheet runoff can influence reserves, money market conditions, and the stability of short-term funding.

[5]

Specific example

Recent policy communications have explicitly linked rate decisions and balance sheet decisions (including concluding certain runoff plans),

highlighting that “Fed policy” is a package deal, not a single dial.

[5]

Also: liquidity facilities matter when markets get quirky. When year-end funding pressure shows up, tools like the Standing Repo Facility can become a pressure valve.

That may sound boring, but “boring plumbing” is what keeps financial systems from turning into a surprise slip-and-slide.

[6]

What to watch

- Policy rate path (cuts, pauses, or hikes) and how the Fed frames “risk”

- Balance sheet policy and reserve conditions

- Money market stress indicators (repo rates, SOFR dynamics, facility usage)

5) Automated investing: the “relentless bid” era grows up

Investing has become more systematized. Index funds, target-date funds, model portfolios, automatic rebalancing, recurring contributions, and robo-advisers

have turned a lot of investing into a background processlike autopay, but for your retirement.

[1][7][8][9]

Why this matters going forward

When more money flows into markets via rules-based systems (instead of vibes-based guesses), the market’s micro-behavior can shift:

fewer panic sellers, more steady buyers, more “buy the dip” by defaultsometimes without even meaning to.

Passive vehicles have also grown so large that the active/passive balance itself becomes a market structure story.

[7][8]

Specific example

Data from major industry trackers shows passive strategies have reached (and in some measures surpassed) active strategies in total assetsan inflection point

that has been building for years.

[7]

Regulation also adapted to this world. The SEC modernized ETF regulation through rulemaking designed to create a clearer framework for most ETFs,

and regulators have issued guidance to help investors understand robo-adviser models, risks, and limitations.

[9]

What to watch

- Flows into index funds, ETFs, and target-date funds

- Growth of options-based and systematic strategies

- How market structure and liquidity behave during stress events

6) Demographics: the slow-motion force that doesn’t stop

Demographics are like gravity: not exciting on a day-to-day basis, but incredibly hard to ignore over decades.

The United States is aging, and that shift changes saving patterns, retirement withdrawals, housing demand, healthcare spending,

and what “risk tolerance” looks like at the population level.

[1][10]

Why this matters going forward

Census projections point to a future with a much larger 65+ population and a changing dependency ratio (more retirees relative to workers).

That can influence everything from Social Security politics to labor supply constraintsboth of which can feed back into inflation and growth.

[10]

Specific example

When the population mix shifts, you can see ripple effects in markets:

more demand for income-oriented assets, more focus on healthcare and services, and more attention to “decumulation” strategies

(how people spend from portfolios, not just build them).

[10]

What to watch

- Population and labor force participation trends

- Retirement policy debates and benefit sustainability

- Intergenerational wealth transfer and saving behavior

7) Inequality: markets aren’t separate from society

Inequality isn’t just a political talking pointit can be a market force.

Why? Because who owns assets, who earns wages, and who has “shock absorbers” (savings, home equity, access to credit)

affects consumer spending, policy decisions, and the stability of economic cycles.

[1][11][13]

Why this matters going forward

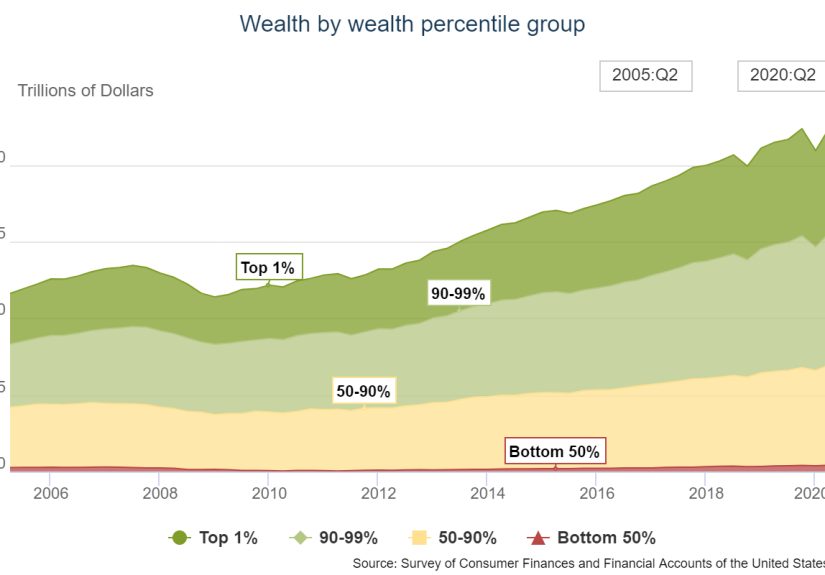

Federal Reserve distributional data shows wealth is heavily concentrated, and that concentration can shape how markets react to downturns.

If the bulk of financial assets sit with households least likely to be forced sellers, sell-offs may be more about fear than necessity.

But if recessions repeatedly hit lower-wealth households hardest, the societal and political pushback can growchanging regulation, taxes,

and the “rules of the game.”

[11][13]

Specific example

Distributional Financial Accounts provide a quarterly view of how aggregate wealth is split across groups.

These data highlight that the bottom half holds a relatively small share of total assets compared with the top groupsan imbalance with real-world implications.

[11]

What to watch

- Wealth and income distribution trends

- Policy responses (tax, regulation, labor market policy)

- Consumer health: credit stress, savings buffers, and affordability

Putting the seven together: a practical market lens

If you want a “markets going forward” checklist that doesn’t require psychic abilities, try this:

- Rates: Are yields rising, falling, or stuckand what does that do to valuations and borrowing?

- Fiscal: Is government policy adding fuel, applying brakes, or just changing the shape of the road?

- Inflation: Are prices cooling, re-heating, or shifting from goods to services?

- The Fed: What’s happening with policy, balance sheet choices, and liquidity conditions?

- Automation: Are flows steady, systematic, and persistentor reversing under stress?

- Demographics: Are long-term population shifts affecting labor, spending, and retirement behavior?

- Inequality: Is asset ownership concentration amplifying social and policy pressure?

Notice what’s missing: “today’s hot take,” “the one weird chart,” and “a guy on the internet who says this time is different.”

The goal isn’t to predict every move. It’s to understand what kind of environment you’re inbecause the environment often matters more than the headline.

Friendly reminder: This is educational market commentary, not personalized financial advice. If you’re making real money decisions,

it’s worth talking to a qualified professional who can account for your goals, timeline, and risk tolerance.

Conclusion

Markets going forward won’t be shaped by one magic variable. They’ll be shaped by a bundle of forces that interact:

rates influence valuations, inflation influences rates, the Fed influences financial conditions, fiscal policy influences growth, demographics influence labor and spending,

and inequality influences everything from consumer resilience to political pressure.

The good news is you don’t need to forecast perfectly to invest well. A “wealth of common sense” approach is to focus on what you can control:

diversification, costs, time horizon, and a plan you can actually stick withespecially when the market is trying to scare you into doing something dramatic.

500-word experiences add-on

Real-World Experiences: How These Seven Forces Show Up (and Mess With People)

If you’ve watched markets for any length of time, you’ve probably noticed a pattern: the “story” changes constantly, but the emotions don’t.

Investors cycle through hope, fear, regret, and the occasional overconfidence that can only be described as “bold, considering the evidence.”

The seven forces above aren’t abstract conceptsthey’re the stuff that people feel in real life.

Start with interest rates. When rates were near zero, a lot of investors got used to the idea that bonds were just there to be… there.

Then yields jumped and suddenly bond prices droppedsurprising people who thought bonds only came in one flavor: “safe.”

The experience taught a painful but useful lesson: bonds can be volatile when rates move fast, and starting yield matters more than most people think.

When yields are higher, the income component becomes a real contributor again, which can change how portfolios behave over time.

[2][12]

Then there’s inflation. Inflation is the force that makes people say, “I got a raise!” and then immediately whisper, “…why does everything cost more?”

In periods where inflation cools, investors often feel relief even if the stock market is choppybecause lower inflation can mean less pressure for rates to rise.

In hotter inflation periods, the vibe shifts: consumers feel squeezed, companies face input cost uncertainty, and markets become hypersensitive to every data release.

[4]

The Fed shows up in experience as “the referee,” even though it’s really managing policy and market plumbing.

When liquidity looks tight or funding markets get weird, people learn quickly that stability isn’t automaticit’s maintained.

Big moments of Fed action can calm markets fast, but they also teach a second lesson: if investors begin to assume rescue is guaranteed,

risk-taking can creep in where it doesn’t belong.

[5][6]

Fiscal stimulus tends to be experienced less through charts and more through the economy’s mood.

When fiscal support is strong, recessions may feel shorter or less severe for many households and businesses.

But persistent deficits can become their own “slow-burn” concern, especially when interest costs rise and political debates intensify.

Markets don’t always react immediatelybut they pay attention when the long-term path begins to constrain choices.

[11]

Automated investing shows up as a quieter experience: people keep investing through payroll contributions and rebalancing rules,

even when they swear they’re “definitely not looking at their account right now.” (They are.)

One of the most interesting shifts of the modern era is that many investors have become more consistent participantssometimes without realizing itbecause the system is built that way.

It doesn’t eliminate fear, but it can reduce the chance that fear immediately becomes action.

[7][9]

Demographics and inequality show up in experience through life stages and resilience.

An aging population means more people thinking about income, healthcare, and retirement timing, which influences how they perceive risk.

Inequality shows up as uneven shock absorption: some households can ride out downturns easily, others can’t.

That unevenness can shape spending, political pressure, and the policy responses that markets eventually need to price in.

[10][11][13]

Put it all together and a common experience emerges: the best investors aren’t the ones who “predict right” every quarter.

They’re the ones who build a plan that survives different regimeshigher rates, lower rates, sticky inflation, changing policy, shifting demographics

without requiring them to reinvent themselves (or their portfolio) every time the market throws a tantrum.