Table of Contents >> Show >> Hide

- First, a quick reality check: “sunk cost” isn’t just a business-school phrase

- The biggest sunk cost: missing the market’s best moments

- The timing tax: five hidden costs investors underestimate

- 1) Cash drag and the lost compounding you don’t see

- 2) Taxes: the cost of being “right” too soon

- 3) Trading friction: spreads, slippage, and “small” costs that add up

- 4) Re-entry risk: you sell low, then buy back higher (because you’re human)

- 5) The psychological bill: decision fatigue and plan drift

- But isn’t market timing sometimes rational?

- Smarter alternatives that avoid the sunk costs

- A practical playbook: how to stop paying the “timing tax”

- Bottom line: timing feels productive, but discipline is profitable

- Experiences From the Real World: How Market Timing Quietly Gets You

- Experience #1: The Cash Pile That Felt Safe (Until It Didn’t)

- Experience #2: The Two-Button Video Game Nobody Wins

- Experience #3: “I’m Not Timing, I’m Just Waiting for a Better Price”

- Experience #4: The Retirement Countdown That Turns Volatility Into Panic

- Experience #5: The “One More Signal” Spiral

Market timing is the financial equivalent of trying to merge onto the freeway by waiting for a “perfect” opening

that never arriveswhile everyone else just… merges and gets where they’re going. Sure, sometimes a timer looks

like a genius. But over a full investing lifetime, the bigger story is usually the tab you don’t notice you’re

running: the sunk costs of market timing.

In this article, we’ll break down the real costsopportunity cost, taxes, trading friction, and the sneaky mental

tollthat pile up when investors hop in and out of the market. We’ll also cover practical, non-headline-driven

alternatives like dollar-cost averaging and rules-based rebalancing that help you stay invested without feeling

like you’re gambling on tomorrow’s news.

Note: This is general educational information, not personalized investment advice.

First, a quick reality check: “sunk cost” isn’t just a business-school phrase

A sunk cost is money, time, or effort you’ve already spent that you can’t recoverregardless of what you do next.

The classic mistake is letting past spending push you into future bad decisions (“I’ve waited this long, I can’t buy now!”),

even though the past is gone either way.

In investing, market timing creates sunk costs in two ways:

- Direct costs you can measure: taxes, transaction costs, bid-ask spreads, fees, and sometimes advisory or platform costs.

- Indirect costs you feel later: missed compounding, missed rebound days, and a growing habit of second-guessing your plan.

The painful part? Many of these costs show up as “nothing happened.” You sat in cash waiting for the perfect entry,

so your statement looks calm… while your long-term growth quietly takes the hit.

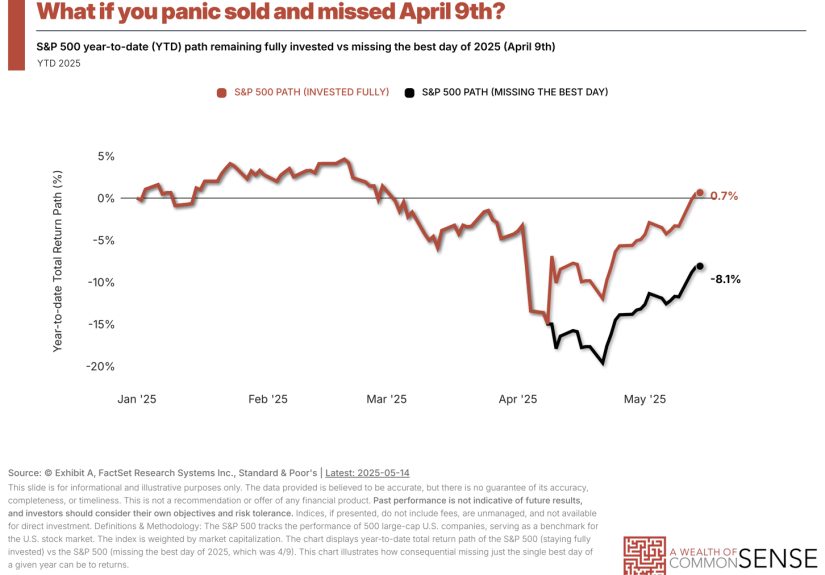

The biggest sunk cost: missing the market’s best moments

The most common argument against market timing isn’t moral (“timing is bad”)it’s mathematical:

big up days matter disproportionately, and they often appear when everything feels terrible.

Why “I’ll get back in when things look better” is so expensive

Many reputable investment research teams have shown some version of the same pattern:

the best days and the worst days tend to cluster during volatile periods.

If you exit during a selloff, you increase the odds you’ll miss the reboundbecause rebounds often arrive while the news still looks ugly.

That’s the market timing trap in plain English: your brain wants confirmation, but markets don’t wait for your comfort.

By the time the headlines feel safe, prices may have already moved.

The “two decisions” problem (and why it’s harder than it sounds)

Market timing isn’t one heroic decision. It’s two:

- When to get out (sell or reduce risk)

- When to get back in (buy again)

Getting one of those right is difficult. Getting both right consistentlyover decadesborders on a full-time job.

And even if you nailed the exit, hesitation on the re-entry can turn your “smart move” into an expensive pause.

The timing tax: five hidden costs investors underestimate

1) Cash drag and the lost compounding you don’t see

Compounding is powerful because it’s boring. It’s also fragile because it needs time.

When you sit out, you’re not just missing “a good week.” You’re potentially missing the early part of a recovery,

which can be the difference between long-term momentum and long-term regret.

Cash has a role (emergency fund, near-term goals). But using cash as a “waiting room” for the perfect market entry

often turns into a long stayespecially if your rule is “I’ll buy when volatility is gone.” Volatility never truly leaves; it just changes outfits.

2) Taxes: the cost of being “right” too soon

Timing strategies can accidentally convert long-term investing into short-term trading. That has consequences:

- Short-term capital gains (often taxed at higher ordinary-income rates in the U.S.) can apply if you sell positions held for a year or less.

- Frequent selling can also create a “tax churn” effectrealizing gains earlier than you otherwise wouldreducing the amount left to compound.

Even when you sell at a loss, timing can create complications. For example, if you sell a security at a loss and buy it back too quickly,

wash sale rules may limit your ability to claim the loss as you intended. (Translation: taxes have their own rules, and they do not care about your vibes.)

3) Trading friction: spreads, slippage, and “small” costs that add up

Modern trading feels cheap. But “commission-free” doesn’t mean “free.”

Bid-ask spreads, market impact, and the subtle price differences between what you wanted and what you got

can stack up when you trade more frequently.

Over decades, repeated friction can quietly erode returnsespecially if your timing strategy involves multiple round trips

during choppy markets (which is exactly when spreads and slippage can sting more).

4) Re-entry risk: you sell low, then buy back higher (because you’re human)

If you sell after a drop, your brain is now looking for proof the drop is “over.”

That proof often appears after prices rise. So investors end up doing the classic two-step:

sell after the fall, buy after the rebound.

This isn’t because investors are foolish. It’s because timing demands emotional precision during emotional moments.

Markets move fast; confidence moves slow.

5) The psychological bill: decision fatigue and plan drift

Market timing is mentally expensive. It turns investing into a constant referendum on your intelligence.

Every headline becomes a test. Every red day becomes a personal insult.

Over time, this creates two behavioral problems:

- Decision fatigue: you make more reactive, lower-quality choices because you’re always “on.”

- Plan drift: your portfolio stops reflecting your goals and starts reflecting your mood.

Ironically, the emotional stress of timing can become a sunk cost that keeps you timing.

You’ve invested so much effort trying to be “right” that it feels hard to stopeven when the evidence says the strategy isn’t helping.

But isn’t market timing sometimes rational?

There’s a reasonable question hiding inside the timing impulse:

“Shouldn’t I reduce risk when things look risky?”

The more durable answer usually isn’t “time the market.” It’s:

align risk with your time horizon and goals.

If you need the money soon, it may not belong in volatile assets in the first place.

If you’re investing for long-term goals (like retirement), then volatility is often part of the price of admission.

A healthy distinction: asset allocation vs. market timing

Adjusting your asset allocation based on life changes (age, income stability, upcoming expenses, risk tolerance)

is not the same as trying to predict next month’s market direction.

Market timing says: “I’m going to outguess the market.”

A sensible allocation says: “I’m going to design a portfolio I can stick with.”

One is a prediction contest. The other is a behavior-friendly system.

Smarter alternatives that avoid the sunk costs

Dollar-cost averaging: consistency that doesn’t require clairvoyance

Dollar-cost averaging (DCA) means investing equal amounts at regular intervals regardless of market ups and downs.

It’s not magic, and it won’t always beat investing a lump sum immediately.

But it can help investors stay engaged and reduce the stress of “choosing the perfect day.”

If market timing is a high-wire act, DCA is taking the stairs. It’s not flashy. It’s reliable. And it gets you where you’re going.

Rules-based rebalancing: buy low and sell high without the drama

Rebalancing is an underappreciated superhero of long-term investing. It forces you to do the thing you claim you want to do:

trim what’s grown, add to what’s fallen.

You can rebalance on a schedule (e.g., annually) or within bands (e.g., when an allocation drifts a set percentage).

The key is that the rule exists before the panic.

Automation: the simplest antidote to headline-driven decisions

Many investors don’t need a new strategythey need fewer opportunities to sabotage themselves.

Automating contributions and keeping a diversified portfolio can reduce the temptation to “do something” every time the market sneezes.

A practical playbook: how to stop paying the “timing tax”

Step 1: Write your “why” before the next selloff

Create a short investing policy statement (IPS). Nothing fancyjust a plain-English note that answers:

What is this money for, and when do I need it?

A good IPS is like a seatbelt: you wear it before you need it.

Step 2: Decide your risk level once, then let it work

Choose an allocation that matches your goals and sleep schedule. If you can’t sleep during volatility,

that’s not a “willpower problem”it’s an allocation problem.

Step 3: Use pre-commitment rules

- Automate contributions (DCA) to reduce “should I buy now?” stress.

- Rebalance with a calendar or bands to keep behavior consistent.

- Limit portfolio check-ins (daily checking is basically emotional day-trading).

Step 4: Keep your emergency fund separate

Many timing mistakes are actually anxiety mistakes. A robust emergency fund can prevent you from treating your long-term investments

like a short-term safety net.

Step 5: Focus on what you can control

You can’t control markets. You can control:

savings rate, diversification, costs, taxes (with good planning), and behavior.

Those levers tend to matter more than guessing what the S&P 500 does next Tuesday.

Bottom line: timing feels productive, but discipline is profitable

Market timing sells a comforting story: “If I’m careful enough, I can avoid pain.”

The market’s reality is different: volatility is normal, rebounds are unpredictable, and your biggest edge is often

staying invested long enough for compounding to do its job.

The sunk costs of market timing aren’t just financialthey’re emotional, behavioral, and strategic.

If timing has you stuck in a loop of waiting, reacting, and regretting, the best move may be the simplest:

build a plan you can live with, automate the boring parts, and let time in the market do what it’s been doing for a very long time.

Experiences From the Real World: How Market Timing Quietly Gets You

The “experience” of market timing is rarely one dramatic blow-up. More often, it’s a slow leakdeath by a thousand

reasonable-sounding decisions. Below are common patterns investors describe (illustrative scenarios, not specific people),

and how the sunk costs show up in daily life.

Experience #1: The Cash Pile That Felt Safe (Until It Didn’t)

A classic story goes like this: an investor sells after a scary drop and parks the money in cash “just for now.”

At first, it feels amazinglike stepping indoors during a storm. The problem is that storms don’t end with a polite announcement.

Markets can rebound while headlines still sound miserable, so the investor waits for confirmation that “the coast is clear.”

Weeks turn into months. The portfolio statement looks stable, but the investor’s confidence starts eroding:

“If I buy now and it drops again, I’ll feel stupid.” That’s the psychological sunk costpast fear controlling future action.

Eventually, the investor buys back in after a strong run-up (because it finally “feels safe”).

The hidden cost isn’t just missing a few good days; it’s missing the early phase of compounding that could have mattered for years.

Experience #2: The Two-Button Video Game Nobody Wins

Market timing is like a game with two buttons: Sell and Buy Back.

Many investors discover they can occasionally press one button at the right timebut pressing both correctly is brutal.

Someone sells because valuations look high or recession risk seems obvious. That part can even look smart in hindsight.

Then the re-entry decision arrives… and it’s emotionally harder.

Re-entry often requires buying when things still feel uncertain. If the investor waits for certainty, prices may rise without them.

If they jump back in too early and the market drops again, they feel burned and may sell again.

That creates a churn cycle: sell, hesitate, buy, panic, repeateach loop adding taxes, friction, and stress.

The sunk cost becomes the time and energy spent monitoring markets like a second job, without the paycheck.

Experience #3: “I’m Not Timing, I’m Just Waiting for a Better Price”

This is market timing wearing a trench coat and sunglasses. Investors often say they aren’t timing the market;

they’re just being “patient.” But the definition matters less than the outcome: staying uninvested while waiting for a specific price level.

The most common emotional trigger is regret avoidance: “I don’t want to invest right before a dip.”

Unfortunately, avoiding small regret can invite big opportunity cost. The market doesn’t offer a clean calendar of dips.

It offers random volatilitysometimes up, sometimes down, sometimes both in the same week.

Waiting for a perfect price can mean sitting out a long stretch where the market trends upward in messy, unsatisfying increments.

Experience #4: The Retirement Countdown That Turns Volatility Into Panic

Near retirement, timing temptation often spikes. People see a bad quarter and think,

“I can’t afford another downturn,” so they move heavily to cash. Sometimes that’s appropriateif the allocation was too aggressive

for the time horizon. But often it’s a reactive swing rather than a planned shift.

The sunk cost here is twofold. First, if the market rebounds, the portfolio misses a recovery when it has fewer earning years left

to make up the gap. Second, the investor may lose trust in their own plan. That’s enormous.

When you don’t trust your plan, every market move becomes a reason to change itand that’s how timing becomes a lifestyle.

A more resilient approach is to adjust risk deliberately (years in advance), keep an emergency buffer for near-term spending,

and use rebalancing rules rather than gut reactions.

Experience #5: The “One More Signal” Spiral

Timing strategies often start with a simple rule: “I’ll wait for inflation to drop,” or “I’ll buy when the Fed starts cutting,”

or “I’ll invest once earnings stabilize.” The problem is that each signal has a sequel:

inflation drops but growth looks weak; rates fall but headlines predict recession; earnings stabilize but geopolitics flares up.

There’s always one more reason to wait.

This is where sunk costs become sticky. Investors feel they’ve already done the hard partresearch, waiting, discipline

so they keep waiting to justify the effort. But investing isn’t a test you pass by delaying.

The most repeatable “experience” investors report after stepping away from timing is relief:

less stress, fewer reactive trades, and a portfolio that once again reflects goals instead of breaking news.